As I discussed in my previous posts, "I Was Wrong" and "The SEC Should Ban High Frequency Trading", my stance on HFT has shifted over the past few months. Initially I, like many other fundamental investors, was worried about the dominance of HFT. A simple glance at the massive increases in volume and volatility, the explosion in the number of hedge funds employing quantitative strategies, their AUM increases, and the waterfall of profits they were generating, was an indication to me of the increasing success of their strategies. However, like many things in this world, it could not last forever. Markets are like a natural system, and HFT is part of that system. No matter how successful an element of a system is, it will always mean revert because nothing can escape the laws of physics and economics indefinitely.

As I mentioned in the last post, a lack of competitive barriers would eventually sap the abnormal profitability of HFT strategies as a whole. This seems to have occurred in the near term, as a recent WSJ article indicates that the average profit of HFT strategies has been cut in half from all time highs during the 2008-2010 credit crisis. This may be temporary, however, I believe it is a structural change in the industry that will continue, as evidenced by quants moving from equities to other asset classes. There are only so many active, liquid, and volatile asset classes (the ingredients for a successful HFT strategy). Thus, you can employ game theory to see the end result before it arrives. Too much capital chasing too few profitable trades results in less profit per trade and a normalized distribution of returns, with most players achieving a return within hailing distance of average. The quants will have their days in the sun, but they are no longer infallible.

I think there are very few real barriers to entry in most businesses, and HFT is no exception. All it takes is capital, infrastructure, and a handful of PHD's to put together these strategies. It turns out there is plenty of cheap supply for each part of that equation, and returns for HFT strategies will normalize in the future because of that fact.

Friday, May 6, 2011

Saturday, January 15, 2011

I Was Wrong.

You do not hear many investors saying this statement. In fact, you almost never hear investors saying this statement because it is simply a matter of psychology. Any active investor, myself included, is by definition stating that they are smarter than the person on the other side of the trade. This is clearly not always the case, which is why it is imperative that you learn early on in your investing career when to be persistent in remaining in / increasing a trade and when to pull out. Humility. Understanding and embracing that one word will go a long way in ensuring that you make the right trades for your portfolio. The truth is that the market will humble you at some point in time. The question is whether or not you listen to what it is saying, and more importantly, if you learn from that particular mistake. The greatest investors will admit they were wrong, and then will proceed to pull apart their own mistakes and the mistakes of others in trying to improve their investment process. This is what differentiates the good investor from the average. The good investor focuses on their process of investing, whereas the average investor focuses on the outcomes.

While I have made numerous mistakes in my investment portfolio, one of the ones that I have made on this blog is an entry I wrote in August 2009 entitled "The SEC Should Ban High Frequency Trading". In a very uncharacteristic moment of irrationality, I wrote the blog arguing that the SEC should be more responsible and should disallow HFT. I was wrong. Upon further thought and discussion, it is my contention that the SEC is not well equipped to deal with traders who are have more resources than and are faster and smarter than the market regulator itself. Banning HFT outright is a poor policy response to a natural evolution in the free markets. To disallow progress is to disrupt the very foundation upon which our capitalist system is built. Case in point, the Globe & Mail ran an article today about a new trading system named "Thor" that RBC Capital Markets has been developing for its buy-side clients. This product is designed to deliver much-needed relief to fundamental long-term investors who are getting out-gunned in the markets on a daily basis due to the natural advantages that high frequency trading systems have accorded to the quants and hedgies. This system is basically an evolutionary response by the markets to negate the abilities of HFT, and it appears to work successfully (for now). We do not need more regulation. Like animals in the wild, the markets have evolved and adapted to the hunting strategies of high frequency traders. Economics tells us that abnormal profits will eventually be eroded away through competition. The development of RBC's system is just the first step in the evolution of competition when it comes to HFT. My initial position was wrong. I believe in free markets.

While I have made numerous mistakes in my investment portfolio, one of the ones that I have made on this blog is an entry I wrote in August 2009 entitled "The SEC Should Ban High Frequency Trading". In a very uncharacteristic moment of irrationality, I wrote the blog arguing that the SEC should be more responsible and should disallow HFT. I was wrong. Upon further thought and discussion, it is my contention that the SEC is not well equipped to deal with traders who are have more resources than and are faster and smarter than the market regulator itself. Banning HFT outright is a poor policy response to a natural evolution in the free markets. To disallow progress is to disrupt the very foundation upon which our capitalist system is built. Case in point, the Globe & Mail ran an article today about a new trading system named "Thor" that RBC Capital Markets has been developing for its buy-side clients. This product is designed to deliver much-needed relief to fundamental long-term investors who are getting out-gunned in the markets on a daily basis due to the natural advantages that high frequency trading systems have accorded to the quants and hedgies. This system is basically an evolutionary response by the markets to negate the abilities of HFT, and it appears to work successfully (for now). We do not need more regulation. Like animals in the wild, the markets have evolved and adapted to the hunting strategies of high frequency traders. Economics tells us that abnormal profits will eventually be eroded away through competition. The development of RBC's system is just the first step in the evolution of competition when it comes to HFT. My initial position was wrong. I believe in free markets.

Monday, January 10, 2011

The Risks Inherent With Investing In Warrants - Part 2

So, apparently the security holders of GLW were sufficiently irate enough to launch a formal complaint against the previously announced FNV / GLW deal. As I profiled in my initial blog post, "The Risks Inherent With Investing In Warrants", my analysis indicated that both shareholders and warrant-holders should be unhappy with the deal.:

• Shareholders would be unhappy because they basically received no return on their investment since the IPO (albeit a good premium to recent trading prices). Regardless of my valuation concerns, with the proposed consideration, it would be an incredibly mediocre deal because the split between cash and shares would be exactly 60% / 40% (0.0934 FNV shares and C$2.08 in cash), which means that shareholders that wanted either consideration would only get that specific mix. In short, shareholders that wanted all FNV shares would receive only 60% of their consideration in that form and shareholders that wanted all cash would receive only 40% of their consideration in that form. Most investors would have a preference one way or another, which virtually ensures that all parties would be unhappy with the structure, let alone the valuation.

• Warrant-holders would be unhappy because they were being robbed of their optionality. Given that the consideration to be paid was 40% in cash, the warrants would lose a significant portion of their optionality as they could no longer be exercised into a full FNV share, but rather into the consideration only (cash has no optionality, which is really the only reason one would hold a warrant). Note that this is precisely why GLW warrants dropped so rapidly on December 13th, the day of the acquisition announcement.

On January 6th, 2011, a new deal with revised terms was announced:

• GLW shareholders can elect to receive a) C$5.20 per share in cash or b) 0.1556 FNV common shares, subject to the limitations of a cap on both forms of consideration as well as pro-ration. Total cash available is C$215mm and total shares available are 9.66mm.

• GLW warrants can be exercised for 0.1556 FNV shares or C$5.20 in cash. In essence, the warrant-holders are now not forced to swallow a 60% / 40% split, but are allowed to choose what form of consideration they want. As cash has zero optionality, in this situation, all warrant-holders would choose FNV shares.

What the revised offer does is it gives security-holders the option to select a form of consideration that is consistent with their individual needs and desires. In a situation like this, typically all shareholders would opt for the all-cash portion, thereby attaining a fixed price and real and immediate liquidity. Whether or not shareholders choose cash or FNV shares is dependent on their perception of the valuation of FNV (whether it is cheap or dear) and the opportunity costs to each individual investor. Moreover, the new option allows those that wanted to hold onto their GLW shares roll-over their ownership into FNV, whereas those that want to cash out can do so without having to rely on market prices and without causing market impact (which can be an issue for large shareholders trying to move blocks in an illiquid name). With all shareholders electing the all-cash option, this would cause the cash portion of the collar to be breached and all security-holders would receive a pro-rata share of both considerations, equivalent to the original 60% / 40% split. The same result would occur if all shareholders chose the FNV share option. It remains to be seen what GLW shareholders ultimately elect, and I will report on this once the election results are announced. It will be interesting to see what the results are, but like with most deals, I imagine that shareholders will gravitate towards the cash option. In my view, this is especially so because GLW is being valued at around 90% of NAV, whereas FNV is being valued in the market at around 150% of NAV. Moreover, FNV is not a pure-play on gold, but rather a conglomeration of royalty interests in gold, platinum, copper, nickel, oil, and gas. Unless I'm missing something, no rationale investor would agree to trade a position in a discounted pure-play into a position in a relatively over-priced conglomerate. My guess is that shareholders will get a pro-rata share of both considerations as a result of everybody clamoring for the cash option.

To me, what is very interesting is that most deals have to be renegotiated because the valuation is too low. Either shareholders negotiate a bump, force a bump through appraisal rights, or a new bid from another party comes forth. In this case, GLW shareholders were apparently happy with the valuation of the firm. However, warrant-holders (and probably shareholders) were unhappy in terms of the type consideration that would be paid. That is not the fault of the security-holders, but rather it is the fault of management. In essence, the forced re-jigging of this deal was really because of poor security-holder communication on behalf of management. It appears that GLW completed the deal in a hasty fashion, and did not fully consider its security-holders wants or needs, nor fully understand the market micro-structure of its securities. Luckily for warrant-holders, GLW management was smart enough to renegotiate the deal, and hopefully all parties can walk away from this averted debacle satisfied.

• Shareholders would be unhappy because they basically received no return on their investment since the IPO (albeit a good premium to recent trading prices). Regardless of my valuation concerns, with the proposed consideration, it would be an incredibly mediocre deal because the split between cash and shares would be exactly 60% / 40% (0.0934 FNV shares and C$2.08 in cash), which means that shareholders that wanted either consideration would only get that specific mix. In short, shareholders that wanted all FNV shares would receive only 60% of their consideration in that form and shareholders that wanted all cash would receive only 40% of their consideration in that form. Most investors would have a preference one way or another, which virtually ensures that all parties would be unhappy with the structure, let alone the valuation.

• Warrant-holders would be unhappy because they were being robbed of their optionality. Given that the consideration to be paid was 40% in cash, the warrants would lose a significant portion of their optionality as they could no longer be exercised into a full FNV share, but rather into the consideration only (cash has no optionality, which is really the only reason one would hold a warrant). Note that this is precisely why GLW warrants dropped so rapidly on December 13th, the day of the acquisition announcement.

On January 6th, 2011, a new deal with revised terms was announced:

• GLW shareholders can elect to receive a) C$5.20 per share in cash or b) 0.1556 FNV common shares, subject to the limitations of a cap on both forms of consideration as well as pro-ration. Total cash available is C$215mm and total shares available are 9.66mm.

• GLW warrants can be exercised for 0.1556 FNV shares or C$5.20 in cash. In essence, the warrant-holders are now not forced to swallow a 60% / 40% split, but are allowed to choose what form of consideration they want. As cash has zero optionality, in this situation, all warrant-holders would choose FNV shares.

What the revised offer does is it gives security-holders the option to select a form of consideration that is consistent with their individual needs and desires. In a situation like this, typically all shareholders would opt for the all-cash portion, thereby attaining a fixed price and real and immediate liquidity. Whether or not shareholders choose cash or FNV shares is dependent on their perception of the valuation of FNV (whether it is cheap or dear) and the opportunity costs to each individual investor. Moreover, the new option allows those that wanted to hold onto their GLW shares roll-over their ownership into FNV, whereas those that want to cash out can do so without having to rely on market prices and without causing market impact (which can be an issue for large shareholders trying to move blocks in an illiquid name). With all shareholders electing the all-cash option, this would cause the cash portion of the collar to be breached and all security-holders would receive a pro-rata share of both considerations, equivalent to the original 60% / 40% split. The same result would occur if all shareholders chose the FNV share option. It remains to be seen what GLW shareholders ultimately elect, and I will report on this once the election results are announced. It will be interesting to see what the results are, but like with most deals, I imagine that shareholders will gravitate towards the cash option. In my view, this is especially so because GLW is being valued at around 90% of NAV, whereas FNV is being valued in the market at around 150% of NAV. Moreover, FNV is not a pure-play on gold, but rather a conglomeration of royalty interests in gold, platinum, copper, nickel, oil, and gas. Unless I'm missing something, no rationale investor would agree to trade a position in a discounted pure-play into a position in a relatively over-priced conglomerate. My guess is that shareholders will get a pro-rata share of both considerations as a result of everybody clamoring for the cash option.

To me, what is very interesting is that most deals have to be renegotiated because the valuation is too low. Either shareholders negotiate a bump, force a bump through appraisal rights, or a new bid from another party comes forth. In this case, GLW shareholders were apparently happy with the valuation of the firm. However, warrant-holders (and probably shareholders) were unhappy in terms of the type consideration that would be paid. That is not the fault of the security-holders, but rather it is the fault of management. In essence, the forced re-jigging of this deal was really because of poor security-holder communication on behalf of management. It appears that GLW completed the deal in a hasty fashion, and did not fully consider its security-holders wants or needs, nor fully understand the market micro-structure of its securities. Luckily for warrant-holders, GLW management was smart enough to renegotiate the deal, and hopefully all parties can walk away from this averted debacle satisfied.

Wednesday, January 5, 2011

M&A In 2010

As a quick follow up to my post of February 8th, 2010 entitled "2009 vs 2010: Developments In The M&A Market", I wanted to touch on how M&A actually played out in 2010. As you can see from the recently released Dealogic League Table below, both Goldman and Morgan Stanley came in 1st and 2nd (or vice versa, depending on how it is counted), as I initially predicted. In addition, the dealers that received very large amounts of TARP (Citi and BoA / Merrill in particular) slid in the rankings. Their loss came at the gain of large international dealers such as UBS and Credit Suisse. Moreover, other international dealers such as Deutsche Bank, BNP Paribas, Nomura, and HSBC all moved up in the rankings at the expense of smaller US-focused boutique firms. Part of this has to do with a trend that I did not foresee, which was the massive expansion in M&A activities in emerging markets - specifically Asia. Earlier in the year, there were numerous reports of various firms racing to open up shop in Shanghai and other financial hubs in the East.

From a global perspective, it looks like there was $2.25 trillion worth of deals done in 2010, up for the first time since 2007. With liquidity taps opening and credit markets easing, corporate acquirers were clearly on the hunt in 2010, which is basically in line with what I expected. It is a trend that I expect will continue in 2011. On sector basis, O&G and telecom did quite well, as expected.

I'll be back shortly to expand further on my expectations of M&A in 2011.

From a global perspective, it looks like there was $2.25 trillion worth of deals done in 2010, up for the first time since 2007. With liquidity taps opening and credit markets easing, corporate acquirers were clearly on the hunt in 2010, which is basically in line with what I expected. It is a trend that I expect will continue in 2011. On sector basis, O&G and telecom did quite well, as expected.

I'll be back shortly to expand further on my expectations of M&A in 2011.

Friday, December 24, 2010

The Risks Inherent With Investing In Warrants

I thought I would write a quick post on the risks with investing in warrants, because the practical risks are not always discussed in finance courses or textbooks. In fairness, the thought to write a post on this topic was borne out of an article posted on The Financial Post a few days ago with respect to the Franco-Nevada Mining / Gold Wheaton acquisition that was recently announced. It provides an instructive example and lesson as to why warrants are inherently risky - especially for those deciding to go long outright.

On December 13th, it was announced that Franco-Nevada Mining would acquire Gold Wheaton by way of Plan of Arrangement for 0.0934 Franco-Nevada shares per Gold Wheaton share and $2.08 in cash consideration. In sum, the consideration would total $5.20 per GLW share, equivalent to a one day 19% premium, and a 60% / 40% split in favour of FNV shares and cash.

As an initial shareholder of GLW (which came into existence in its current form in June 2008), I would not be happy at all in the sense that the original over-subscribed equity raise was for $260mm (with green shoe) at $5.00 for subscription receipts (after a 10 for 1 share consolidation in February 2010) that included one GLW share and a 1/2 warrant struck at $10.00 for 5 years. In my estimation, the value of the 1/2 warrant was anywhere from $0.65 to $1.00 in additional consideration. This deal was well oversubscribed, and you can see the demand for this issue as the stock price tripled in value in the span of a few months (see graph below). The most startling thing is that they were able to issue the 1/2 warrants at 100% ups, which I guess is offset by the fact that each warrant had five years of time to expiration. Typically, in Canada, the strike price is about 20-40% higher than where the underlying is currently trading, and the warrants have an expiry of 18 to 24 months after the deal closes. In hindsight, I do understand why this deal was over-subscribed, and ultimately upsized, with all the brokers and management buying in as well. Any way you slice it, it was a very attractive deal for anybody that bought, which is partly why the stock rifled higher afterwards in the secondary market.

Immediately after the acquisition by FNV was announced, GLW started trading at $5.10 and GLW.WT started trading at $0.28 (see graph above). As a buyer of the sub-receipts on July 8th, 2008 for $5.00, the consideration I am getting out of this deal once it is all wrapped up is approximately $5.20 - a laughable 4% return over the span of approximately 2 years and 8 months. Note that the consideration calculation assumes the FNV portion remains constant (in reality FNV's shares will fluctuate slightly) and the public warrant holders get nothing because they are far out of the money. Moreover, as you can see from the chart below, GLW was being valued quite low by the market. The two charts below were taken from a GLW corporate presentation that was done on November 9th. Given the trading price of the stock, GLW's NAV is approximately $5.65, which means that FNV is only paying 92% of NAV - still a massive discount to where the comps are trading at. So, to clarify, GLW is being valued too low on an absolute and relative basis. Now, the original deal was well supported with players such as GMP, Paradigm, FNX, Sprott, Frank Guistra, and various other insiders buying in, so I am baffled as to how this deal got done because unless they sold when the stock was $10 or $15 (which was only a period of 5 months, under which they were mostly under lock-up), it seems to me that nobody has made any money!

From the perspective of a GLW warrant holder, I would not be happy. First, as an instructional, warrant values are driven off of three main inputs - the underlying share price, the volatility priced into the shares / market by traders, and the inherent time to maturity negotiated into the warrant indenture. Typically it is the former two that drive the pricing of the warrants on a day-to-day basis, as the latter is whittled down slowly as time passes. Let's look at what happened in the case of GLW warrants in the context of this deal.

• Stock Price - In an acquisition, the stock price rifles upwards on announcement of the deal. This is obviously positive for a warrant as part of its value is derived from the stock price. It does depend on where the stock price is in relation to the warrant's strike price. If the value of the consideration offered is less than the strike price, the warrant is basically worthless because it has no intrinsic value and limited time value. In the case of GLW, the publicly traded warrants had a strike price of $10.00, and therefore they will ultimately have zero value once the deal is completed.

• Time To Maturity - The longer the time to maturity, the greater the value of the warrant because it has more time to become "in the money". In the context of the GLW deal, the time maturity shrinks massively, thereby destroying the value of the warrant. Prior to the deal being announced, the warrant had 939 days left until expiry. After the deal was announced, the warrant had 108 days to expiry under a worst case scenario (assuming the deal is wrapped up by the end of March). In one fell swoop, 88.5% of the time that the warrant had left to expiry was eliminated because of the acquisition. This is what we call "event risk" and that is the first explanation for why the warrants dropped in price from $0.57 to $0.28 the day after the announcement, and settled in at $0.17 thereafter.

• Volatility - Prior to an acquisition, a stock price trades freely based on fundamentals and sentiment. After an acquisition, a stock trades in relation to the acquisition price and usually moves very little. If it does move, it is based on the assessment of the deal getting done. In essence, the volatility in the stock evaporates because the stock has no reason to gyrate in response to macro-economic reasons, industry changes, or even company specific developments, etc. It only moves based on news flow related to the deal and supply and demand from the arbs, which means that the stock will typically move very little. Although it would have been more prevalent in a case where the warrants were in the money, in the case of GLW warrants, volatility dropped significantly (see the post-acquisition announcement trading price graph below) and the price of the warrants in the open market cratered. In the case of an acquisition, because both time to maturity and volatility are drastically reduced, it is a little difficult to estimate what portion of the value reduction was attributable to which lever, especially because volatility is imputed from the price of the stock. However, once again, from the graph below you can visually see that volatility of the underlying GLW shares has disappeared.

Now, if you run the black-scholes model, you'll find that the theoretical price of GLW warrants is actually around 2-3 cents, yet the market has priced them anywhere from $0.15 to $0.29 post-deal announcement, and has traded them in decent volume. I'm not quite sure why anybody would pay so much over their theoretical value, but my guess is that it is simply speculators that are trading for a few pennies of profit here and there.

The other grating aspect of being long warrants of a company that is being acquired is that even if you are hedged (by shorting the stock), because volatility - the primary driver of a "warrant volatility" strategy - drops like a rock, your warrant goes down more in percentage terms than the stock you shorted.

Although this post has largely been about the negative aspects of warrants, it is important to understand the fundamentals as to how these types of securities work, and oftentimes that is best learned through losing money (such as GLW warrant holders did). On the flip side, warrants provide a significant amount of leverage and are fantastic ways to make money very rapidly, if you can navigate the minefield and buy and sell at the right time. This is especially true with warrants because time is constantly working against you when you employ such a strategy.

In Canada, there are approximately 162 public warrant issues outstanding currently, and there are probably hundreds of warrant issues that trade hands privately. In short, there are a lot of long-dated derivative ways to make money in the Canadian markets. One of my goals in the new year is to rebuild my database of warrants with updated terms. I think with the VIX currently toeing 15-16, there is a good chance to put on some attractive warrant volatility trades in the near term. It is just a matter of sorting through the rubble to find the gems. Time to add that to my New Years resolutions list.

On December 13th, it was announced that Franco-Nevada Mining would acquire Gold Wheaton by way of Plan of Arrangement for 0.0934 Franco-Nevada shares per Gold Wheaton share and $2.08 in cash consideration. In sum, the consideration would total $5.20 per GLW share, equivalent to a one day 19% premium, and a 60% / 40% split in favour of FNV shares and cash.

As an initial shareholder of GLW (which came into existence in its current form in June 2008), I would not be happy at all in the sense that the original over-subscribed equity raise was for $260mm (with green shoe) at $5.00 for subscription receipts (after a 10 for 1 share consolidation in February 2010) that included one GLW share and a 1/2 warrant struck at $10.00 for 5 years. In my estimation, the value of the 1/2 warrant was anywhere from $0.65 to $1.00 in additional consideration. This deal was well oversubscribed, and you can see the demand for this issue as the stock price tripled in value in the span of a few months (see graph below). The most startling thing is that they were able to issue the 1/2 warrants at 100% ups, which I guess is offset by the fact that each warrant had five years of time to expiration. Typically, in Canada, the strike price is about 20-40% higher than where the underlying is currently trading, and the warrants have an expiry of 18 to 24 months after the deal closes. In hindsight, I do understand why this deal was over-subscribed, and ultimately upsized, with all the brokers and management buying in as well. Any way you slice it, it was a very attractive deal for anybody that bought, which is partly why the stock rifled higher afterwards in the secondary market.

Immediately after the acquisition by FNV was announced, GLW started trading at $5.10 and GLW.WT started trading at $0.28 (see graph above). As a buyer of the sub-receipts on July 8th, 2008 for $5.00, the consideration I am getting out of this deal once it is all wrapped up is approximately $5.20 - a laughable 4% return over the span of approximately 2 years and 8 months. Note that the consideration calculation assumes the FNV portion remains constant (in reality FNV's shares will fluctuate slightly) and the public warrant holders get nothing because they are far out of the money. Moreover, as you can see from the chart below, GLW was being valued quite low by the market. The two charts below were taken from a GLW corporate presentation that was done on November 9th. Given the trading price of the stock, GLW's NAV is approximately $5.65, which means that FNV is only paying 92% of NAV - still a massive discount to where the comps are trading at. So, to clarify, GLW is being valued too low on an absolute and relative basis. Now, the original deal was well supported with players such as GMP, Paradigm, FNX, Sprott, Frank Guistra, and various other insiders buying in, so I am baffled as to how this deal got done because unless they sold when the stock was $10 or $15 (which was only a period of 5 months, under which they were mostly under lock-up), it seems to me that nobody has made any money!

From the perspective of a GLW warrant holder, I would not be happy. First, as an instructional, warrant values are driven off of three main inputs - the underlying share price, the volatility priced into the shares / market by traders, and the inherent time to maturity negotiated into the warrant indenture. Typically it is the former two that drive the pricing of the warrants on a day-to-day basis, as the latter is whittled down slowly as time passes. Let's look at what happened in the case of GLW warrants in the context of this deal.

• Stock Price - In an acquisition, the stock price rifles upwards on announcement of the deal. This is obviously positive for a warrant as part of its value is derived from the stock price. It does depend on where the stock price is in relation to the warrant's strike price. If the value of the consideration offered is less than the strike price, the warrant is basically worthless because it has no intrinsic value and limited time value. In the case of GLW, the publicly traded warrants had a strike price of $10.00, and therefore they will ultimately have zero value once the deal is completed.

• Time To Maturity - The longer the time to maturity, the greater the value of the warrant because it has more time to become "in the money". In the context of the GLW deal, the time maturity shrinks massively, thereby destroying the value of the warrant. Prior to the deal being announced, the warrant had 939 days left until expiry. After the deal was announced, the warrant had 108 days to expiry under a worst case scenario (assuming the deal is wrapped up by the end of March). In one fell swoop, 88.5% of the time that the warrant had left to expiry was eliminated because of the acquisition. This is what we call "event risk" and that is the first explanation for why the warrants dropped in price from $0.57 to $0.28 the day after the announcement, and settled in at $0.17 thereafter.

• Volatility - Prior to an acquisition, a stock price trades freely based on fundamentals and sentiment. After an acquisition, a stock trades in relation to the acquisition price and usually moves very little. If it does move, it is based on the assessment of the deal getting done. In essence, the volatility in the stock evaporates because the stock has no reason to gyrate in response to macro-economic reasons, industry changes, or even company specific developments, etc. It only moves based on news flow related to the deal and supply and demand from the arbs, which means that the stock will typically move very little. Although it would have been more prevalent in a case where the warrants were in the money, in the case of GLW warrants, volatility dropped significantly (see the post-acquisition announcement trading price graph below) and the price of the warrants in the open market cratered. In the case of an acquisition, because both time to maturity and volatility are drastically reduced, it is a little difficult to estimate what portion of the value reduction was attributable to which lever, especially because volatility is imputed from the price of the stock. However, once again, from the graph below you can visually see that volatility of the underlying GLW shares has disappeared.

Now, if you run the black-scholes model, you'll find that the theoretical price of GLW warrants is actually around 2-3 cents, yet the market has priced them anywhere from $0.15 to $0.29 post-deal announcement, and has traded them in decent volume. I'm not quite sure why anybody would pay so much over their theoretical value, but my guess is that it is simply speculators that are trading for a few pennies of profit here and there.

The other grating aspect of being long warrants of a company that is being acquired is that even if you are hedged (by shorting the stock), because volatility - the primary driver of a "warrant volatility" strategy - drops like a rock, your warrant goes down more in percentage terms than the stock you shorted.

Although this post has largely been about the negative aspects of warrants, it is important to understand the fundamentals as to how these types of securities work, and oftentimes that is best learned through losing money (such as GLW warrant holders did). On the flip side, warrants provide a significant amount of leverage and are fantastic ways to make money very rapidly, if you can navigate the minefield and buy and sell at the right time. This is especially true with warrants because time is constantly working against you when you employ such a strategy.

In Canada, there are approximately 162 public warrant issues outstanding currently, and there are probably hundreds of warrant issues that trade hands privately. In short, there are a lot of long-dated derivative ways to make money in the Canadian markets. One of my goals in the new year is to rebuild my database of warrants with updated terms. I think with the VIX currently toeing 15-16, there is a good chance to put on some attractive warrant volatility trades in the near term. It is just a matter of sorting through the rubble to find the gems. Time to add that to my New Years resolutions list.

Monday, December 20, 2010

Novartis Versus Alcon - A Win For Alcon's Minority Shareholders And Minority Shareholder Rights

As I had previously discussed the Novartis / Alcon deal in a post entitled '"Majority of the Minority": A Simple Remedy for Minority Squeeze-Outs', I thought I would give a quick update on the outcome of the deal.

On December 15th, Novartis announced that it had come to terms with the Board of Directors of Alcon, and proposed a deal to acquire the remaining 23% stake in Alcon it did not already own from minority shareholders (http://invest.alconinc.com/phoenix.zhtml?c=130946&p=irol-pressReleasesArticle&ID=1507867&highlight=). The reason why this is important is because the history of the deal extends for several years, and Novartis initially attempted to squeeze out minority shareholders for significantly less consideration than it paid for the controlling stake it acquired in Alcon from Nestle. This was a significant win for minority shareholders, as Novartis had no such obligation to give them as much consideration as Nestle under Swiss securities law. Here is a brief outline of what occurred:

• April 7th, 2008 - Novartis acquired a 25% stake in Alcon from Nestle for $143.18 in cash consideration. The deal had some interesting provisions worked in, whereby Novartis had the option to acquire Nestle's remaining 52% stake by a certain date at a certain price.

• January 4th, 2010 - Novartis exercised its call option to acquire Nestle's remaining 52% stake for $180 in cash consideration. Simultaneously, Novartis made an offer to minority shareholders for $153 in the form of an all-share offer of 2.8 Novartis shares. The first issue was that the offer was lower in monetary terms. The second issue was that it was in shares, which although technically fungible with cash, are worth less than an all-cash offer because they created uncertainty of what a minority shareholder would receive in the end. Moreover, the deal was further complicated because Novartis shares are priced in Swiss Francs, which introduced exchange rate risk for a minority shareholder. In short, the offer was inadequate any way you looked at it. Luckily, the three independent directors of Alcon formed a committee to review the transaction.

• January 20th, 2010 - Alcon's independent committee determined that the deal was "grossly" inadequate.

• February 17th, 2010 - RiskMetrics publicly stated that the Novartis deal was prejudicial to Alcon minority shareholders.

• July 8th, 2010 - Alcon's independent committee created a $50mm "litigation trust" that allowed them to continue to legally protect minority shareholder rights upon the acquisition of Nestle's 52% stake by Novartis.

• December 15th, 2010 - After a little over 11 months, Novartis folded their hand and agreed to acquire the remaining 23% in Alcon for a price of $168 per share. This is payable with 2.8 Novartis shares, and if the value of the share consideration falls short at closing, then it will be topped up to $168 with cash. The $168 consideration is basically the blended price that Nestle received for its two blocks of shares.

As always, there is some commentary that I would like to make. First and foremost, I find this deal to be bittersweet for minority shareholders. It is a positive outcome to this deal in the sense that the deal is finally getting done. It is negative in the sense that it has been a long time between the initial offer in January and the closing of the deal will be over a year, and closer to a year and a half once the legalities are wrapped up. Alcon shareholders have been in limbo, and will continue to be this way for the next few months.

Secondly, the bump in consideration from $153 to $168 is also positive. However, the consideration is in shares, which any appraiser can tell you are less valuable than cash. It is true that it will be a "tax free" rollover for shareholders, so they have the option of holding onto their stake without tax consequences. However, cash is a certainty and should always be valued higher than shares. Share values are transient. They are typically supported by fundamentals in the long-term, but can deviate significantly in the short-term. The other aspect of this transaction is that if the value of the offer comes in at more than $168 at closing, the share ratio will be reduced to ensure consideration remains at $168. Although I am skeptical of Novartis' share price rallying much higher prior to deal closing (due to hedging), the attractiveness of the consideration received will only be certain on the closing date. At current prices, Novartis is trading at 14x earnings, which is at the higher range of comparables, although not outrageous on an absolute basis. What I would be worried about as a potential Novartis shareholder is multiple compression, and more importantly, fund managers selling their newly acquired Novartis shares on the open market after the closing date, thereby depressing the price. In short, the consideration received is uncertain, and there is some probability of it being less than $168.

Third, the $168 is a blended price that Nestle received in total. It is a combination of an initial $143.18 on the 25% stake sold in 2008 and $180 on the 52% stake sold in 2010. I maintain that the $143.18 price was a trade done in the context of a different market and at a different time. As such, it is irrelevant to the pricing of any stake being sold in 2010. Moreover, the value of the Alcon business was different in 2008 than in 2010. I believe that the minority shareholders should have argued for $180, as they should receive the same consideration that Nestle received in 2010. At the very least they should have argued for an interest adjustment on the $143.18 portion, as Nestle effectively had access to that cash two years prior. My solution would have been to apply some sort of risk-free interest rate (t-bill or short-dated treasuries) to the $143.18 portion of the consideration calculation to bring the value of the cash to present value. Using one month US t-bills as the proxy, the additional consideration would amount to about $0.31 or 20 basis points more than what Novartis offered, primarily because rates cratered over the 2 year time frame. Although the methodology is more fair and correct (in my view), this option was probably not considered due to the minor amounts involved and the relative negotiating positions of Novartis and Alcon. On the flip side, I do understand that there is a control premium ascribed to Nestle's 52% block of shares, which minority shareholders cannot take part in. This is the main "bitter" aspect of the deal. The shares are probably worth $180, but minority shareholders have no legal way to force a bump. Nor can they argue that they deserve the price ascribed to a control block. Given that the independent committee has recommended that shareholders approve the deal, I believe it will go through as planned.

Fourth, I must applaud the independent board of directors for taking the steps necessary to fight for minority shareholder rights. The $15 increase in consideration for the 69mm shares held by minority shareholders translates into a little over $1bn in additional value that is rightfully theirs. That is the product of three individuals fighting for minority shareholders, but a slew of other parties as well. Both proxy advisory firms, Glass Lewis and RiskMetrics were instrumental in guiding the market to refuse Novartis' "grossly inadequate" initial offer.

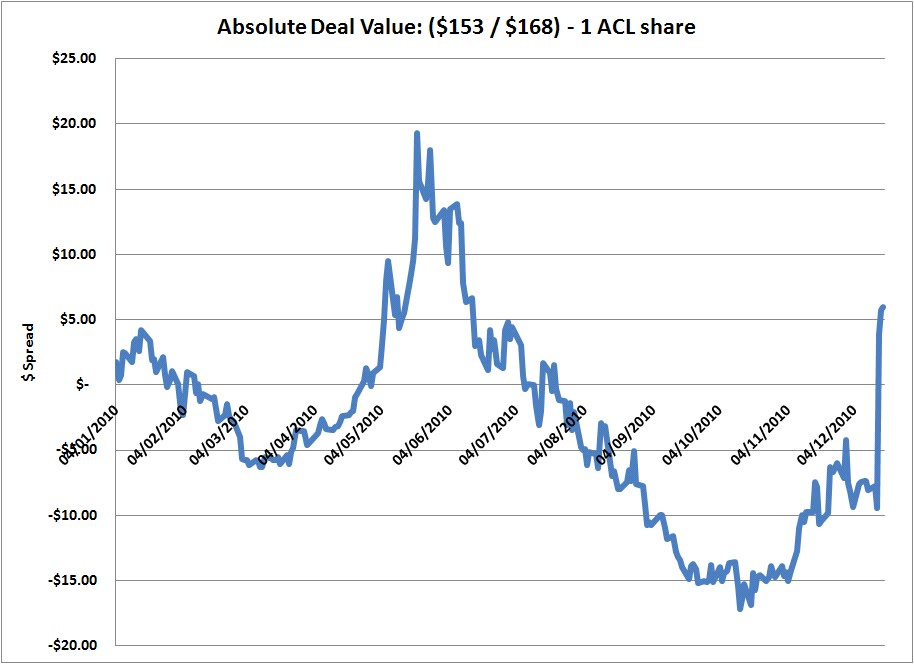

Fifth, as indicated by market folly's recent post, this deal will get done because of the fact that the arbs are now deep into this trade and will vote in favour. I wanted to point out visually how the market responded to this deal throughout time.

The graph shown above displays the spread value on a relative basis. What I mean by this is the spread value of the deal originally announced (the value of 2.8 NVS shares minus the value of 1 ACL share). As you can see, the market immediately priced a negative spread on the deal, as it believed that minority shareholders should get closer to $180 for their shares. Three things are playing out here. First, the ACL shares are initially being hedged with NVS shares as arbs have to short 2.8 NVS for each 1 ACL they own. That put tremendous pressure on the price of NVS in the market, thus lowering the value of the share consideration immediately. This is in addition to the share dilution concern by NVS shareholders who would have sold NVS for that reason alone. Second, as markets began to tumble in the summer, NVS shares had more pressure on them which pushed the value of the share consideration down even further and the expectation of a bump in the share exchange ratio up. Hedgies would look at the value of the share consideration at $135 and say that it is too low relative to the already low absolute valuation of $153 that was set by NVS only 6 months prior (keeping in mind there is relatively little change in the fundamental value of the business). They would also assume that they are getting a free option on a bump in the share exchange ratio, and would thus put on the spread at +$5 all the way up to $20. Third, as market participants talk and determine what the real value of the minority stake is and the likelihood of a bump, their expectations for a bump increase simultaneously (along with the risk trade being put back on in August) and they begin to push the value of ACL shares from the $150's into the $160's. The interesting aspect of this is two-fold. First, given what market folly indicated in his post, the hedgies could have been colluding to go long at the same time and thus affect the status of the deal (a form of quasi-activism). The second interesting aspect is that as soon as the stock continues to hang at the $160 level for an extended amount of time, it is clear to any market participant that NVS will be forced to offer more consideration if it wants to close the deal - in essence, the bump is a self-fulfilling prophecy. You can see this in the chart below. From August onwards, the deal traded at a negative spread (assuming a $153 payout), with ACL rallying all the way to $170, presumably under the assumption by some poor-sap that a deal would get done at $180. It promptly sold off to a more reasonable level in the low 160's when NVS decided to bump to $168 to get the deal done.

Sixth, strategic deals like this always get done in the end. Novartis is primarily concerned with acquiring and running the business for fundamental / strategic reasons. They could not continue to fight to oppress minority shareholders because they have the business to run as control investors. I understand that they tried to take advantage of minority shareholders, however, I am just baffled at how long it took for them to work out the deal. You can clearly see them integrating the business as time goes on (appointment of Novartis CFO to oversee Alcon, appointment of Novartis CEO to chair Alcon, etc), so you can see their thought process playing out in the press releases, and it was apparent to me that they were going to do the deal at some point in time. Why did it take eleven months? I guess we'll never know.

Seven, it took NVS approximately 8 months to acquire Nestle's 52% stake, and my assumption is that it will take a shorter time frame to acquire the minority stake held by the public. The company has guided to "the first half of 2011" in terms of closing, which makes it a 6 month long wait until consideration is paid out, assuming a worst case scenario. I think there is a chance it could get done sooner. From a risk-arb perspective, that is a long time to have your capital at risk, which will not be attractive to all arbs. The share price of ACL should stay within hailing distance of $168. At the current price of $161.70, the annualized return is roughly 8%, which is about right for this type of trade. I think ACL has to trade down to $157 or $158 to make it attractive currently. With that said, I think there will be an opportunity at some point in time to go long ACL at an attractive annualized return (+15%). Given the volatility in the markets and the skittishness of arbs, there is a good chance of ACL being sold off in the coming months due to the risk trade being taken off by funds. As it stands right now, I'm a buyer at $158.

On December 15th, Novartis announced that it had come to terms with the Board of Directors of Alcon, and proposed a deal to acquire the remaining 23% stake in Alcon it did not already own from minority shareholders (http://invest.alconinc.com/phoenix.zhtml?c=130946&p=irol-pressReleasesArticle&ID=1507867&highlight=). The reason why this is important is because the history of the deal extends for several years, and Novartis initially attempted to squeeze out minority shareholders for significantly less consideration than it paid for the controlling stake it acquired in Alcon from Nestle. This was a significant win for minority shareholders, as Novartis had no such obligation to give them as much consideration as Nestle under Swiss securities law. Here is a brief outline of what occurred:

• April 7th, 2008 - Novartis acquired a 25% stake in Alcon from Nestle for $143.18 in cash consideration. The deal had some interesting provisions worked in, whereby Novartis had the option to acquire Nestle's remaining 52% stake by a certain date at a certain price.

• January 4th, 2010 - Novartis exercised its call option to acquire Nestle's remaining 52% stake for $180 in cash consideration. Simultaneously, Novartis made an offer to minority shareholders for $153 in the form of an all-share offer of 2.8 Novartis shares. The first issue was that the offer was lower in monetary terms. The second issue was that it was in shares, which although technically fungible with cash, are worth less than an all-cash offer because they created uncertainty of what a minority shareholder would receive in the end. Moreover, the deal was further complicated because Novartis shares are priced in Swiss Francs, which introduced exchange rate risk for a minority shareholder. In short, the offer was inadequate any way you looked at it. Luckily, the three independent directors of Alcon formed a committee to review the transaction.

• January 20th, 2010 - Alcon's independent committee determined that the deal was "grossly" inadequate.

• February 17th, 2010 - RiskMetrics publicly stated that the Novartis deal was prejudicial to Alcon minority shareholders.

• July 8th, 2010 - Alcon's independent committee created a $50mm "litigation trust" that allowed them to continue to legally protect minority shareholder rights upon the acquisition of Nestle's 52% stake by Novartis.

• December 15th, 2010 - After a little over 11 months, Novartis folded their hand and agreed to acquire the remaining 23% in Alcon for a price of $168 per share. This is payable with 2.8 Novartis shares, and if the value of the share consideration falls short at closing, then it will be topped up to $168 with cash. The $168 consideration is basically the blended price that Nestle received for its two blocks of shares.

As always, there is some commentary that I would like to make. First and foremost, I find this deal to be bittersweet for minority shareholders. It is a positive outcome to this deal in the sense that the deal is finally getting done. It is negative in the sense that it has been a long time between the initial offer in January and the closing of the deal will be over a year, and closer to a year and a half once the legalities are wrapped up. Alcon shareholders have been in limbo, and will continue to be this way for the next few months.

Secondly, the bump in consideration from $153 to $168 is also positive. However, the consideration is in shares, which any appraiser can tell you are less valuable than cash. It is true that it will be a "tax free" rollover for shareholders, so they have the option of holding onto their stake without tax consequences. However, cash is a certainty and should always be valued higher than shares. Share values are transient. They are typically supported by fundamentals in the long-term, but can deviate significantly in the short-term. The other aspect of this transaction is that if the value of the offer comes in at more than $168 at closing, the share ratio will be reduced to ensure consideration remains at $168. Although I am skeptical of Novartis' share price rallying much higher prior to deal closing (due to hedging), the attractiveness of the consideration received will only be certain on the closing date. At current prices, Novartis is trading at 14x earnings, which is at the higher range of comparables, although not outrageous on an absolute basis. What I would be worried about as a potential Novartis shareholder is multiple compression, and more importantly, fund managers selling their newly acquired Novartis shares on the open market after the closing date, thereby depressing the price. In short, the consideration received is uncertain, and there is some probability of it being less than $168.

Third, the $168 is a blended price that Nestle received in total. It is a combination of an initial $143.18 on the 25% stake sold in 2008 and $180 on the 52% stake sold in 2010. I maintain that the $143.18 price was a trade done in the context of a different market and at a different time. As such, it is irrelevant to the pricing of any stake being sold in 2010. Moreover, the value of the Alcon business was different in 2008 than in 2010. I believe that the minority shareholders should have argued for $180, as they should receive the same consideration that Nestle received in 2010. At the very least they should have argued for an interest adjustment on the $143.18 portion, as Nestle effectively had access to that cash two years prior. My solution would have been to apply some sort of risk-free interest rate (t-bill or short-dated treasuries) to the $143.18 portion of the consideration calculation to bring the value of the cash to present value. Using one month US t-bills as the proxy, the additional consideration would amount to about $0.31 or 20 basis points more than what Novartis offered, primarily because rates cratered over the 2 year time frame. Although the methodology is more fair and correct (in my view), this option was probably not considered due to the minor amounts involved and the relative negotiating positions of Novartis and Alcon. On the flip side, I do understand that there is a control premium ascribed to Nestle's 52% block of shares, which minority shareholders cannot take part in. This is the main "bitter" aspect of the deal. The shares are probably worth $180, but minority shareholders have no legal way to force a bump. Nor can they argue that they deserve the price ascribed to a control block. Given that the independent committee has recommended that shareholders approve the deal, I believe it will go through as planned.

Fourth, I must applaud the independent board of directors for taking the steps necessary to fight for minority shareholder rights. The $15 increase in consideration for the 69mm shares held by minority shareholders translates into a little over $1bn in additional value that is rightfully theirs. That is the product of three individuals fighting for minority shareholders, but a slew of other parties as well. Both proxy advisory firms, Glass Lewis and RiskMetrics were instrumental in guiding the market to refuse Novartis' "grossly inadequate" initial offer.

Fifth, as indicated by market folly's recent post, this deal will get done because of the fact that the arbs are now deep into this trade and will vote in favour. I wanted to point out visually how the market responded to this deal throughout time.

The graph shown above displays the spread value on a relative basis. What I mean by this is the spread value of the deal originally announced (the value of 2.8 NVS shares minus the value of 1 ACL share). As you can see, the market immediately priced a negative spread on the deal, as it believed that minority shareholders should get closer to $180 for their shares. Three things are playing out here. First, the ACL shares are initially being hedged with NVS shares as arbs have to short 2.8 NVS for each 1 ACL they own. That put tremendous pressure on the price of NVS in the market, thus lowering the value of the share consideration immediately. This is in addition to the share dilution concern by NVS shareholders who would have sold NVS for that reason alone. Second, as markets began to tumble in the summer, NVS shares had more pressure on them which pushed the value of the share consideration down even further and the expectation of a bump in the share exchange ratio up. Hedgies would look at the value of the share consideration at $135 and say that it is too low relative to the already low absolute valuation of $153 that was set by NVS only 6 months prior (keeping in mind there is relatively little change in the fundamental value of the business). They would also assume that they are getting a free option on a bump in the share exchange ratio, and would thus put on the spread at +$5 all the way up to $20. Third, as market participants talk and determine what the real value of the minority stake is and the likelihood of a bump, their expectations for a bump increase simultaneously (along with the risk trade being put back on in August) and they begin to push the value of ACL shares from the $150's into the $160's. The interesting aspect of this is two-fold. First, given what market folly indicated in his post, the hedgies could have been colluding to go long at the same time and thus affect the status of the deal (a form of quasi-activism). The second interesting aspect is that as soon as the stock continues to hang at the $160 level for an extended amount of time, it is clear to any market participant that NVS will be forced to offer more consideration if it wants to close the deal - in essence, the bump is a self-fulfilling prophecy. You can see this in the chart below. From August onwards, the deal traded at a negative spread (assuming a $153 payout), with ACL rallying all the way to $170, presumably under the assumption by some poor-sap that a deal would get done at $180. It promptly sold off to a more reasonable level in the low 160's when NVS decided to bump to $168 to get the deal done.

Sixth, strategic deals like this always get done in the end. Novartis is primarily concerned with acquiring and running the business for fundamental / strategic reasons. They could not continue to fight to oppress minority shareholders because they have the business to run as control investors. I understand that they tried to take advantage of minority shareholders, however, I am just baffled at how long it took for them to work out the deal. You can clearly see them integrating the business as time goes on (appointment of Novartis CFO to oversee Alcon, appointment of Novartis CEO to chair Alcon, etc), so you can see their thought process playing out in the press releases, and it was apparent to me that they were going to do the deal at some point in time. Why did it take eleven months? I guess we'll never know.

Seven, it took NVS approximately 8 months to acquire Nestle's 52% stake, and my assumption is that it will take a shorter time frame to acquire the minority stake held by the public. The company has guided to "the first half of 2011" in terms of closing, which makes it a 6 month long wait until consideration is paid out, assuming a worst case scenario. I think there is a chance it could get done sooner. From a risk-arb perspective, that is a long time to have your capital at risk, which will not be attractive to all arbs. The share price of ACL should stay within hailing distance of $168. At the current price of $161.70, the annualized return is roughly 8%, which is about right for this type of trade. I think ACL has to trade down to $157 or $158 to make it attractive currently. With that said, I think there will be an opportunity at some point in time to go long ACL at an attractive annualized return (+15%). Given the volatility in the markets and the skittishness of arbs, there is a good chance of ACL being sold off in the coming months due to the risk trade being taken off by funds. As it stands right now, I'm a buyer at $158.

Saturday, October 16, 2010

Long Trade Idea - Pollard Banknote Limited

I love researching small and micro-caps because I always seem to find treasure amongst what is perceived as the trash. These businesses are never covered in the media or by analysts, and they are often dirt cheap for a reason. Analytically I find it more stimulating to be able to research these companies than to take for granted what 20 analysts have said about a large-cap bank or oil stock. Risk-reward wise, these small firms also tend to have a lot more upside than larger companies, as evidenced by the small-cap performance advantage discussed in many academic studies.

One of the micro-cap companies that I researched in the summer was Pollard Banknote Limited. I researched it primarily for my own investing purposes, but I also gave a presentation to the Ivey Finance club on why it should be bought. Below, please find the Media Fire link to the PowerPoint presentation, which has audio embedded. In addition, for anybody that does not have the time to watch the presentation, I have done a quick write-up on the investment thesis below that. Enjoy!

http://www.mediafire.com/?gb529c90u9iu52a

Founded in 1907 by the Pollard family (73.3% majority owner), Pollard Banknote (TSX: PBL, $2.50 share price, $16mm float) is in the lottery business. Specifically, Pollard is in three business lines:

1. Instant scratch tickets (88% of revenues) – Pollard produces 10.3bn / annum.

2. Charitable gaming (11% of revenues) – These are essentially pull-tab tickets.

3. Vending machines (1% of revenues) – Vending machines that dispense scratch tickets.

Pollard sells to 45 lotteries world-wide, and generates 56% of its revenues from the US, 24% from Canada, and 20% internationally. They have about 20% market share globally, but 83% in Canada and 20% in the US.

• PBL IPO’d in 2005 as a trust at $10 and has traded down to a low of $2.24. I believe the shares have stabilized at the current level of $2.50. In essence there is limited downside, and I believe this is so because of the cheap valuation and stable business results that it can generate.

• PBL underperformed for five years due to volatile top-line growth, competitive industry pressures, a decline in very volatile earnings, two distribution cuts, a 50% increase in long-term debt since the IPO, and the fact that no research analysts cover it. In short, it is an un-loved, under-followed value stock.

• Since converting into a corporation in May 2010, the dividend is now stable at $0.12 / annum, translating into a 4.8% yield. You are paid to wait for this company to reach a higher, more appropriate valuation.

• Gross margins have always been stable at ~20%. Net margins have fluctuated, but have averaged around 6%. They have trended downwards to about 4% recently. EBITDA margins have stabilized at 12% on a normalized basis. The key take-away? The business is stable, and this is especially so because PBL is part of what is essentially a duopoly in North America.

• PBL trades at 35% of book value and 7x 2010E P/E. It can get cheaper, but I believe it has bottomed based on fundamentals.

• Management rationalized a new $8.5mm press-line installed in 2008 / 2009. It took two years to attain proper efficiencies, so the costs associated with that will no longer be present going-forward. In addition, with the closure of the Kamloops facility, a $4.7mm restructuring charge was assumed in recent quarters, but this will save $4mm in costs per annum in the future. This cost reduction will go directly to the bottom-line and into shareholder’s pockets.

• As capacity utilization is cut (Kamloops), and costs eliminated from the business, growth cap-ex will be cut which will free up the $10-$15mm of free cash flow that the business generates on a normalized basis for debt pay-down. By paying down the $75mm (out of $105mm) credit facility already drawn, the financial / bankruptcy risk of this business will dissipate rather quickly, and I think the market will begin to value PBL slightly higher.

• Taking into account the above mentioned cost-reduction measures, normalized earnings should be around $0.50 / annum. Applying current EV/EBITDA and P/E multiples to the more appropriate forward earnings produces share price targets of $3.40 to $4.00, implying 40% to 60% upside. This does not include contract wins, which are all upside.

• Ultimately, I believe management will privatize the 26.7% of the business it doesn’t own at $3.50 to $4.00, as those are private market values at 7-8x earnings, and represent a 12.5% to 15% earnings yield on the business. Very attractive from an insider's perspective. The final point is that management owns 73.3% of this company. It has been in the family for 103 years. Furthermore, the livelihood and reputation of four Pollard brothers depends on this firm. They will not risk the company by levering it up anymore. Rather, I believe they will take it private and start paying down debt to achieve a higher private-market valuation for the company.

One of the micro-cap companies that I researched in the summer was Pollard Banknote Limited. I researched it primarily for my own investing purposes, but I also gave a presentation to the Ivey Finance club on why it should be bought. Below, please find the Media Fire link to the PowerPoint presentation, which has audio embedded. In addition, for anybody that does not have the time to watch the presentation, I have done a quick write-up on the investment thesis below that. Enjoy!

http://www.mediafire.com/?gb529c90u9iu52a

Founded in 1907 by the Pollard family (73.3% majority owner), Pollard Banknote (TSX: PBL, $2.50 share price, $16mm float) is in the lottery business. Specifically, Pollard is in three business lines:

1. Instant scratch tickets (88% of revenues) – Pollard produces 10.3bn / annum.

2. Charitable gaming (11% of revenues) – These are essentially pull-tab tickets.

3. Vending machines (1% of revenues) – Vending machines that dispense scratch tickets.

Pollard sells to 45 lotteries world-wide, and generates 56% of its revenues from the US, 24% from Canada, and 20% internationally. They have about 20% market share globally, but 83% in Canada and 20% in the US.

• PBL IPO’d in 2005 as a trust at $10 and has traded down to a low of $2.24. I believe the shares have stabilized at the current level of $2.50. In essence there is limited downside, and I believe this is so because of the cheap valuation and stable business results that it can generate.

• PBL underperformed for five years due to volatile top-line growth, competitive industry pressures, a decline in very volatile earnings, two distribution cuts, a 50% increase in long-term debt since the IPO, and the fact that no research analysts cover it. In short, it is an un-loved, under-followed value stock.

• Since converting into a corporation in May 2010, the dividend is now stable at $0.12 / annum, translating into a 4.8% yield. You are paid to wait for this company to reach a higher, more appropriate valuation.

• Gross margins have always been stable at ~20%. Net margins have fluctuated, but have averaged around 6%. They have trended downwards to about 4% recently. EBITDA margins have stabilized at 12% on a normalized basis. The key take-away? The business is stable, and this is especially so because PBL is part of what is essentially a duopoly in North America.

• PBL trades at 35% of book value and 7x 2010E P/E. It can get cheaper, but I believe it has bottomed based on fundamentals.

• Management rationalized a new $8.5mm press-line installed in 2008 / 2009. It took two years to attain proper efficiencies, so the costs associated with that will no longer be present going-forward. In addition, with the closure of the Kamloops facility, a $4.7mm restructuring charge was assumed in recent quarters, but this will save $4mm in costs per annum in the future. This cost reduction will go directly to the bottom-line and into shareholder’s pockets.

• As capacity utilization is cut (Kamloops), and costs eliminated from the business, growth cap-ex will be cut which will free up the $10-$15mm of free cash flow that the business generates on a normalized basis for debt pay-down. By paying down the $75mm (out of $105mm) credit facility already drawn, the financial / bankruptcy risk of this business will dissipate rather quickly, and I think the market will begin to value PBL slightly higher.

• Taking into account the above mentioned cost-reduction measures, normalized earnings should be around $0.50 / annum. Applying current EV/EBITDA and P/E multiples to the more appropriate forward earnings produces share price targets of $3.40 to $4.00, implying 40% to 60% upside. This does not include contract wins, which are all upside.

• Ultimately, I believe management will privatize the 26.7% of the business it doesn’t own at $3.50 to $4.00, as those are private market values at 7-8x earnings, and represent a 12.5% to 15% earnings yield on the business. Very attractive from an insider's perspective. The final point is that management owns 73.3% of this company. It has been in the family for 103 years. Furthermore, the livelihood and reputation of four Pollard brothers depends on this firm. They will not risk the company by levering it up anymore. Rather, I believe they will take it private and start paying down debt to achieve a higher private-market valuation for the company.

Tuesday, October 5, 2010

Money Never Sleeps

Money may never sleep, but I was damn close during this movie. Ever since I first heard about Oliver Stone doing a sequel, I was excited about the chance to see Bud Fox and Gordon Gekko back in action. Alas, just like many other sequels, it did not live up to the precedent set by its predecessor, nor the high expectations set by every fan of the original Wall Street. It was also about 30 minutes too long.

First, Shia LaBeouf? Really? They could not get any better actor than the guy from Transformers? I’ll give it to him that he was mildly believable, but I still can’t get the picture of him running around with giant robots out of my head. *tsk tsk*, Oliver Stone. Poor casting job.

Secondly, the overt references to Lehman, Goldman, Bernanke, et al. By trying to make it so similar to the players and events that actually occurred during the financial crisis, it honestly felt contrived - especially so soon after the events occurred. Given that I didn’t really live through the LBO boom and corporate raider phenomenon, I wonder if the original Wall Street seemed as contrived to people that truly experienced the 1980’s Wall Street? Moreover, the forced inclusion of Bud Fox was a travesty. Bud Fox should have either been a main character or not included at all. Regardless, the cameo was forced and there was not an ounce of chemistry or connection between Fox and Gekko like there rightfully should have been.

Third, and worst of all, Oliver Stone made Gekko cry. Let me repeat. He made Gekko cry. This is supposed to be a character with a heart of stone that would kill for a dollar. Although he was supposed to be the villain in the original Wall Street, he really was the hero to every guy in finance. Part of what made Gekko so great was that he was so twisted. He was everything a normal human being isn’t. He was the guy who didn’t care about humanity, who made gobs of money, who traded size, and got whatever he wanted. In short, he always won. Winners don't cry.

Despite the movie’s shortcomings, I will say that it did have a few highlights. For example, when Gekko is sitting in his new offices in London with his newly formed team and you see that he turned the expropriated $100mm into $1bn. That one minute scene was enough to change the course of the entire movie and put a smile on anyone’s face. Although we never knew how the original Wall Street ended up, we all knew that Gekko was doomed at the end of it. We then waited 23 years for our hero to dig himself out of his hole and rebound to the top again. In that moment when Gekko’s net worth hits 10 figs, the antagonist of both movies rose to become the protagonist for the second time, and it gave all Bay / Wall Street guys that rare feeling that compels our minds and drives our bodies on a daily basis. Not just the feeling of winning. The feeling of winning BIG. Yes, ladies and gentlemen. Greed is still good.

The second best part of the movie was the wardrobe. The tailored suits were impeccable. See below for proof.

First, Shia LaBeouf? Really? They could not get any better actor than the guy from Transformers? I’ll give it to him that he was mildly believable, but I still can’t get the picture of him running around with giant robots out of my head. *tsk tsk*, Oliver Stone. Poor casting job.

Secondly, the overt references to Lehman, Goldman, Bernanke, et al. By trying to make it so similar to the players and events that actually occurred during the financial crisis, it honestly felt contrived - especially so soon after the events occurred. Given that I didn’t really live through the LBO boom and corporate raider phenomenon, I wonder if the original Wall Street seemed as contrived to people that truly experienced the 1980’s Wall Street? Moreover, the forced inclusion of Bud Fox was a travesty. Bud Fox should have either been a main character or not included at all. Regardless, the cameo was forced and there was not an ounce of chemistry or connection between Fox and Gekko like there rightfully should have been.

Third, and worst of all, Oliver Stone made Gekko cry. Let me repeat. He made Gekko cry. This is supposed to be a character with a heart of stone that would kill for a dollar. Although he was supposed to be the villain in the original Wall Street, he really was the hero to every guy in finance. Part of what made Gekko so great was that he was so twisted. He was everything a normal human being isn’t. He was the guy who didn’t care about humanity, who made gobs of money, who traded size, and got whatever he wanted. In short, he always won. Winners don't cry.

Despite the movie’s shortcomings, I will say that it did have a few highlights. For example, when Gekko is sitting in his new offices in London with his newly formed team and you see that he turned the expropriated $100mm into $1bn. That one minute scene was enough to change the course of the entire movie and put a smile on anyone’s face. Although we never knew how the original Wall Street ended up, we all knew that Gekko was doomed at the end of it. We then waited 23 years for our hero to dig himself out of his hole and rebound to the top again. In that moment when Gekko’s net worth hits 10 figs, the antagonist of both movies rose to become the protagonist for the second time, and it gave all Bay / Wall Street guys that rare feeling that compels our minds and drives our bodies on a daily basis. Not just the feeling of winning. The feeling of winning BIG. Yes, ladies and gentlemen. Greed is still good.

The second best part of the movie was the wardrobe. The tailored suits were impeccable. See below for proof.

Monday, October 4, 2010

China: Communism to Capitalism

In May, I had the pleasure of travelling throughout China and Hong Kong with 32 of my classmates from Ivey. The purpose of Ivey’s China Study Trip is to complement the extensive in-class knowledge gained from our GLOBE module. This module focuses on the increasingly global nature of business and includes topics such as economics, international trade, technology, government and public policy, entrepreneurship, and corporate governance. China has been splashed all across the headlines over the past few years as a model of growth and a case-in-point when it comes to the success of globalization. Reading about it is one thing, however, experiencing it is another thing altogether. Although China and globalization is generally outside the purview of this blog, I thought it appropriate to write about my experiences.

One aspect of the trip I really enjoyed was having the opportunity to read the newspapers in China - South China Morning Post and The China Daily. I was amazed at the depth and breadth of activity that is going on in these economies. In North America, we hear only about the high level activity, such as China growing its GDP at +8% for decades or the undervaluation of the Yuan relative to the USD. These tidbits of information are great for a macro perspective on China, but they do little to help one understand the context and the nitty-gritty details of why and how this is all occurring. For that, you have to see for yourself by visiting the country, talking to business-people, and by reading the newspaper.

Here is a small list of the things that I witnessed in the newspaper and in person during my two weeks in China and Hong Kong:

• In one issue of the newspaper, I saw four separate capital raises totaling billions of (converted) Canadian dollars alone. In comparison, the new equity issue market is practically dead in Canada, and I was astounded that one of the Chinese equity issues was 38x over-subscribed! This demonstrates how much appetite for investment opportunities there is in China.

• Pepsi decided to spend $2.5bn over three years to build new plants and expand R&D efforts in China. This piece of information is further proof of international firms making strategic investments and building out their capabilities in China.

• China celebrated the one month anniversary of index futures trading on the newly formed CSI 300 Index, an index of 300 large-cap stocks that trade on the Shenzhen and Shanghai stock exchanges. The establishment of Chinese stock futures demonstrates the financial liberalization that is occurring daily.

• Beijing announced a goal of eliminating smoking inside all public establishments. This data point really highlighted to me how progressive the Chinese government is. It realizes that for it to reach G7 status and become a true super-power, it must make dramatic and sweeping changes to its society.

• Probably most telling of China's economic rise to power, is the symbolism contained in the picture below. While I was there, an exact replica of Wall Street’s Charging Bull statue was unveiled on the Bund in Shanghai.