Do you want to know what really grinds my gears? Opportunity costs. That moment we have all experienced - when a stock that has been on your watch list for the past year suddenly receives an offer to be acquired or jumps +20% in a day. That moment when you realize that all that work you did in the interim seemingly goes down the tubes because you can no longer act on your research at an attractive price. For me, that moment has been replayed over and over in the past five months, as so many of the stocks that I wish I had bought have doubled and / or tripled. The last stock to contribute to the continued crushing of my spirit was Cossette Communications Group (TSX: KOS), a stock that I have been following for quite a while. It has been in a downward spiral for years, and I have been watching it fall further and further, knowing that one day its fortunes would rebound. Aside from the cheap valuation which initially attracted me, I saw KOS as a company with several corporate governance issues (dual class share structure, insider dealings, and board independence issues specifically) and a business under temporary pressure given its economically sensitive revenue streams. If the corporate governance issues could be fixed and advertising spending stabilized, I believed that we could easily see the stock in the high single-digits. While none of that has played out, the day of reckoning came yesterday, as the company received an unsolicited proposal to be acquired by Cosmos Capital by way of Takeover Bid for C$4.95 per subordinate voting share - a 52% premium over the previous day's closing price.

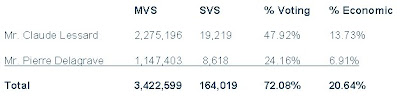

Cosmos Capital is an entity controlled by Mr. François Duffar, a former director of KOS, who resigned effective June 1st, 2009. Other investors include George Morin, Jean Monty, Daniel Bernard, and an un-named multi-billion dollar private equity group. Mr. George Morin, another KOS director, officially tendered his resignation as of July 18th, which just became known yesterday by way of a KOS press release. Together with Mr. Claude Lessard and Mr. Pierre Delagrave, the four members of the Board

held all of the multiple voting shares, which essentially gave them an 85.9% voting interest in the firm, but only 37.9% economic ownership. However, once Duffar and Morin left the board, their MVS were automatically converted into SVS, leaving the main ownership structure as follows:

Now, with Duffar and Morin owning 3.1mm SVS, their voting interest is 6.5%, but their economic interest is 18.6%, which represents the second largest block of shares after Lessard and Delagrave (assuming they are aggregated). On a side note, Burgundy Asset Management owns 1.9mm SVS, representing a 3.99% voting interest and 11.37% economic ownership.

Now this is interesting, as you can see a power struggle emerging between four colleagues who have (had) high positions in management and on the board, and who essentially control the firm via their MVS. Given that the stock has traded at the C$4.95 Takeover Bid price on announcement day (and in fact traded at C$5.15 to close the day) shows that the market and specifically merger-arbitrage players believe that there is more upside to this story. In fact, today, the stock traded mostly above C$5.00, and closed at C$5.20, albeit on small volume (72,000 shares traded). This may indicate that speculative retail players are buying up here. I would expect higher volume created from arbitrageurs buying below the C$4.95 level.

The truth is that it does not take a genius to figure out that Cosmos Capital is trying to pick up the company on the cheap, as one only has to take a cursory look at the facts to see this (http://www.cossette.com/investors/pdf/inv_Factsheet_KOS_20090506.pdf). Looking at EV / normalized EBITDA shows that Cosmos Capital is proposing to pay ~3x. If you factor in cap-ex to get a basic FCF, we are looking at 3 to 4x EV / FCF, which is still extremely cheap. It is reasonable to assume that the range of EPS in a normalized operating environment is anywhere from $0.50 to $0.90, which implies that Cosmos is attempting to pay anywhere from 5.5x to 9.9x earnings, which despite the high premium on 30 day VWAP and previous day closing price, is not much of a valuation premium. While not entirely comparable due to size and geographic diversity, the comps (Interpublic, WPP, and Omnicom) are trading at 11 to 12x trailing EPS. It is also important to keep in mind that these are bottom cycle EPS numbers as well, so there is certainly room for upside for any acquiror. Aside from these basic valuation measures, the best information to look at in this situation would be media (specifically advertising company) acquisition premiums and valuation metrics, however I am not a media analyst, so I do not have enough historic information to do a proper analysis. My gut instinct and the information I do have tells me that this proposal is inadequate, and we will see the newly formed special committee either force a higher bid from Cosmos or another party (likely Lessard) via an auction process.

While I do believe a higher bid will be forthcoming, there are a few caveats for anybody wishing to play this from a merger-arbitrage perspective. First off, this is only a proposed Takeover-Bid, which means this is a risk because no deal is actually on the table as of yet. In addition, because Cosmos Capital technically already owns an 18.7% position in the stock, you must be aware that they have already benefited from the jump in the stock price, and this is before anything other than the proposal has occurred. Therefore, they may have ulterior motives and it wise to be aware of that possibility. Secondly, Burgundy Asset Management owns an 11.1% economic interest in the firm, and Cosmos has convinced them to sign a "hard lock-up" agreement, meaning that they cannot sell their shares below the C$4.95 bid, unless a higher bid is tabled. This is important because it means that 30% of the shares, yet only 10.4% of the votes, are in favor of the deal from the get-go. Although I have never been in favour of the dual class share structure, this is exactly why it was created, as Lessard and Delagrave now have an extremely valuable blocking position. Finally, my biggest hesitation in playing this deal is that I do not have a read on what Lessard is thinking. He is the largest shareholder, and he was clearly kept out of Cosmos Capital's bid, which may have irritated him and may cause him to reject their bid outright. This is important because he controls a 47.4% voting interest in the company, and therefore can block any proposal he wants. (66 2/3% is the generally the required amount for a Takeover Bid to close). It is also important to note that the firm is essentially his baby, as he started his career at KOS in 1972 as President & CEO, and has built it into what it is today. So, does he actually want to sell the firm now and at the price Cosmos is offering? Also, does he want to sell to ex-colleague's that went behind his back with a Takeover Bid in an attempt to "steal" his company from him? My guess is no. He is also the most incentivized person in terms of seeing a higher stock price, so my guess is that he will 1) have the special committee search for a higher bid (this is obvious) or 2) emerge as a bidder himself. From 1996 to 2008 he has received salary and bonus compensation of anywhere from $600,000 to $1,000,000 per annum, and as he has held his same position since 1972, he likely had a similar compensation scheme from 1972 to 1996 (adjusted for inflation). My point is that he is likely wealthy enough to arrange his own bid in some way, shape, or form.

Regardless of the risks to this proposal, I am still positive on a deal materializing, however, at the +C$5.00 level, buying shares now leaves no room for error. Given that KOS is now a risk-arb situation as opposed to just a cheap stock, the risk / return parameters have changed. As such, I would remain on the sidelines until this becomes an official bid, and until you have a chance to read the Takeover Bid circular. In addition, I would be a buyer at a positive spread - likely at the C$4.75 level. This is equivalent to a 21% annualized return according to my deal timeline assumptions, and it takes into account the risk of Lessard using the "just say no" defense. Unfortunately, it does not look like KOS is going to get to that level anytime soon.

So, to circle back to the beginning of this post, the best thing we can do is learn from our mistakes and move on. So the question becomes what did I learn from this missed opportunity?

My take-aways are three-fold:

- When you do your homework, you must believe in your analysis, and must be ready to pull the trigger when an opportunity comes your way.

- The sense of loss I felt upon finding out about the Takeover Bid for KOS was natural. It is only human nature to feel remorse over a potential gain when I had the desire and ability to buy KOS, but did not. It is also natural that this feeling is stronger than an actual monetary loss on a stock, because as humans, we feel that once we have made the decision to buy, the "fate" of the stock is now out of our control, and therefore we attribute this loss to the markets and not ourselves. Conversely, it is interesting that should that stock have gone up after our purchase, the majority of us would attribute it to our savvy investment skills, and not the stock's "fate". Regardless, these feelings are behavioral in nature, and we have to learn to combat them because they can and will lead to mistakes.

- The physical matters. By this, I mean it is vitally important that as analysts, we look through the DCFs and EPS and all the other investment jargon. We have to look at the tangible aspects of a business, because sometimes there are physical clues that sit right in front of our eyes. With respect to KOS, this clue emerged on March 2nd, 2009 when KOS issued a press release announcing that Mr. Francois Duffar, the Vice-Chairman of the Board of Directors and a member of the management team of KOS since 1972, decided to terminate his employment with the firm as of June 1st. While management turnover is normal (especially for someone who has had a 37 year career with the same firm), it is the fact that this action caused his MVS to be automatically converted to SVS. This is what should have tipped me off that something was in the works. In my view, no rational person would willingly give up the control premium that typically comes with MVS, and certainly not without getting something in return. On May 11th, it was announced that Duffar would step down from the Board of Directors, effective that day. This was another hint that I should have picked up on instantly. Fast-forward 70 days, and the stock is up 65.5%, which on Duffar's 2.09mm SVS, represents a paper gain of C$4.1mm, and in my view, the recouping of the control premium he rightfully possessed on his MVS. The physical matters...

{kind=link}