With closing of the Takeover Bid on November 6th, one day later than my estimate of November 5th, the PAR deal has worked out wonderfully for anybody that bought in, even after my initial write up on September 6th.

Shareholders made out extremely well, as they cleared C$7.65 per share in cash consideration on November 6th. They also received one common share of Parex Resources (PXT.V), which was originally valued at C$3.00 when the deal was announced. Markets have recovered quite substantially since then, as PXT started trading four days after deal close at C$3.65, a full 22% above the company’s original valuation. Note that PXT, being inherently more risky and volatile than PAR’s producing assets, actually touched a high of C$4.63 since then, and most recently closed at C$3.95. That is a 32% return on the stub in the span of a little over 3 months, and highlights why arbitrageurs and value investors LOVE spin-offs.

If that was not enough, a holder of the common stock also received 1/10th of a 30 day warrant on PXT, with a strike price at C$3.00 and an expiry of December 6th, 2009. On December 4th, the last day of trading prior to the expiry date, PXT closed at C$3.98, which implies that each share received approximately C$0.098 in additional value that was only accounted for as roughly C$0.025 when the deal was struck four months prior. In essence, while the stub went up 33% in value, the warrant went up 292% in value!

In sum total, shareholders received a minimum estimated value of C$11.40, 99% of which was received by November 12th. Even after my in-depth analysis conducted on September 6th, one could have bought in at C$10.40 and received a 9.6% return, equivalent to a 53% annualized return.

After reading my two posts on PAR, what you should walk away with is how potentially lucrative hostile M&A deals can be, as well as how lucrative spin-offs can be. In addition, I have provided a rudimentary framework from which you can analyze any deals you are personally interested in. On a side note, if you wish to learn more about spin-offs, I highly recommend reading Joel Greenblatt’s book entitled “You Can Be A Stock Market Genius: Uncover The Secret Hiding Places of Stock Market Profits”. Yes, I know, it has a horrible title, however, I can personally attest to the value of the content.

In the next post, I will review the interesting developments at Cossette Communications Group (KOS). In addition, over the Christmas break and throughout 2010, I promise to start writing more material.

Sunday, December 13, 2009

Monday, October 26, 2009

Real Estate & The Ivey Finance Club Newsletter

I realize that my blog contributions have been lacking lately, primarily due to the incredibly tight schedule during the first and second modules for the Ivey MBA program. However, I thought I would write a brief post to highlight a few growth opportunities that I have been afforded within the broader scope of "finance".

Historically speaking, I have always been interested in real estate as a wealth creation vehicle, but have had little opportunity to study the industry or the merits of different types of real estate investments. Thanks to Ivey, this has all changed.

I have had the opportunity to join the Real Estate Club, where every two weeks I have had the chance to gather with like-minded real estate professionals. I have enjoyed our first few meetings, and will continue to network with and learn from this group of talented individuals.

One of our largest projects during the Ivey MBA program is to develop a "New Venture Project" from concept, to business plan, to tangible business. I have been so fortunate to be able to join a group of six bright, young real estate professionals in forming a team. Our firm, entitled "Ivy Green Real Estate Development Corporation", will be a boutique real-estate development firm with a primary focus on mixed-use commercial and residential re-development projects. I am extremely excited to develop our firm concept, and to also be involved in the sourcing of an actual real estate project. I believe actually walking through the concept design, development, and execution of an actual real estate development project with experienced people will give me the framework, confidence, and abilities necessary for building a real estate portfolio in the future.

Finally, as part of the Ivey Finance Club, I have started contributing to the bi-weekly newsletter. Specifically, I am in charge of Real Estate / REIT research. The format is designed to highlight some of the major occurrences in the industry, hone in on a few of those occurrences with some analysis, and then follow up with a few key take-aways / implications.

Historically speaking, I have always been interested in real estate as a wealth creation vehicle, but have had little opportunity to study the industry or the merits of different types of real estate investments. Thanks to Ivey, this has all changed.

I have had the opportunity to join the Real Estate Club, where every two weeks I have had the chance to gather with like-minded real estate professionals. I have enjoyed our first few meetings, and will continue to network with and learn from this group of talented individuals.

One of our largest projects during the Ivey MBA program is to develop a "New Venture Project" from concept, to business plan, to tangible business. I have been so fortunate to be able to join a group of six bright, young real estate professionals in forming a team. Our firm, entitled "Ivy Green Real Estate Development Corporation", will be a boutique real-estate development firm with a primary focus on mixed-use commercial and residential re-development projects. I am extremely excited to develop our firm concept, and to also be involved in the sourcing of an actual real estate project. I believe actually walking through the concept design, development, and execution of an actual real estate development project with experienced people will give me the framework, confidence, and abilities necessary for building a real estate portfolio in the future.

Finally, as part of the Ivey Finance Club, I have started contributing to the bi-weekly newsletter. Specifically, I am in charge of Real Estate / REIT research. The format is designed to highlight some of the major occurrences in the industry, hone in on a few of those occurrences with some analysis, and then follow up with a few key take-aways / implications.

Sunday, September 6, 2009

Enemies To Friends: The Beauty of a Hostile Deal

Although it received little attention in the business news, Petro Andina Resources (TSX: PAR) issued a press release on September 3rd announcing that it had signed a friendly deal to be acquired by Pluspetrol resources, a company that has been pursuing PAR for several months now. The stock immediately jumped 10.50% to ~$10.40, and is now a full 28.6% above the initial Takeover Bid of $8.10 in cash per PAR share. This deal is a wonderful illustration of the beauty of a hostile Takeover Bid, and how when it works right, it can make investors a handsome return in a short period of time. In this blog post, I will go through the history and mechanics of the deal, and how you could have analyzed this situation to end up profiting from it. This deal also exhibits some important underlying principles about investing which I will delve further into throughout the analysis.

DEAL ANALYSIS

First off, the basic history of the deal is shown below:

- June 18th - Pluspetrol Resources bids $8.10 per share in cash consideration for all the outstanding shares of PAR. As per fiduciary duties, PAR's directors announce that they will review the bid and recommend a course of action to shareholders.

- June 19th - Pluspetrol Resources releases the Takeover Bid circular giving all the details of the deal. Specifically, the deal was to expire on August 18th.

- June 22nd - PAR announces that they retained the services of First Energy Capital and Scotia Waterous, two extremely well respected advisory firms in the oil & gas M&A market in Canada.

- July 3rd - PAR releases a Director's Circular which recommends that shareholders reject the Takeover Bid on the basis of fundamental undervaluation (going concern value) , transactions based undervaluation (precedent transactions), opportunistic timing by Pluspetrol, and the possibility of higher value being realized through successful exploration and production.

- July 20th - PAR announces that it has opened up its data rooms to other firms and investors, and has asked for other proposals to be delivered by mid-August, which is very close to the August 18th Bid expiry.

- August 11th - PAR announces 2nd quarter financial results which gives you more updated data, and is useful in getting a better estimate of value.

- August 17th - PAR continues to recommend that shareholders reject the Pluspetrol Takeover Bid. In the press release, they explicitly state that the they have received proposals from other interested parties, and are in the process of negotiations. This is clearly a very good sign.

- August 18th - Pluspetrol announces that it has extended the expiry of its Takeover Bid to September 2nd. At this point, in the back of your mind, you should be thinking that Pluspetrol is serious about PAR, and is not simply going to walk away from its deal.

- September 1st - PAR reiterates its recommendation that shareholders reject Pluspetrol's Takeover Bid.

- September 2nd - Pluspetrol's re-extends its Takeover Bid to September 14th. Once again, we get another hint that Pluspetrol is not walking away.

- September 3rd - Pluspetrol and PAR announce a friendly Plan of Arrangement Agreement, whereby each PAR shareholder would receive C$7.65 in cash per PAR share, one share of a new "exploreco" that would hold PAR's non-producing Colombian and Trinidad & Tobago exploration assets, along with 1/10th of 1 warrant on exploreco struck at $3.00 with expiry 30 days from deal closing. Concurrently, exploreco entered into a bought deal financing for C$16mm at $3.00 / share, with an over-allotment option of $4mm.

Now that we know the history of the deal, we can move on to more important questions that we should have looked at immediately after the announcement of the first deal. To begin with, we must obtain a better handle on the players involved, which will give us an idea of the probability of a deal being consummated:

- Who is Petro Andina? PAR is an E&P firm based out of Calgary that owns 346,000 net acres in the Neuquen Basin in Argentina where it derives all of its production and reserves. It is also exploring in Colombia where it has 489,269 gross acres in undeveloped land and in Trinidad & Tobago where it has 211,000 gross acres of undeveloped land. The company has an internal estimate of net risked resource potential of 20mm boe and 100 boe respectively.

- Who is Pluspetrol Resources? - Pluspetrol Resources is a Dutch private E&P firm with operations in Argentina, Peru, Bolivia, Venezuela, Colombia, and Chile. It has been around since 1977, and started in the Neuquen Basin in Argentina, which is precisely where PAR's Argentina assets are located. As such, we know that this deal is strategic in nature, and Pluspetrol is likely trying to consolidate operations in the Neuquen Basin.

- Can Pluspetrol complete the transaction? As Pluspetrol is a private concern, there is no way of knowing if they are money-good. The main proxy I would use for their ability to pay is their size. Their 2P reserves are ~37.5x the size of PAR, and they produce roughly 23x more on BOE/D basis. Combine that with the fact that they are based out of the Netherlands and operate in no less than 6 other Latin American countries leads me to believe that they have the size, the money, and the ability to access the primary capital markets in Europe and South America, should they need to.

VALUATION

Once you know the basics about the players and their intentions, you must perform a quick analysis of valuation to determine if the assets are being bought at a cheap or expensive price. With the initial bid valued at $8.10 / share, the enterprise value of PAR was ~$347mm. Based on the following fundamentals...

....I developed a table detailing the valuation metrics.

Based on the metrics above, you can clearly tell that PAR was still undervalued after the initial bid. This would be even more clear based on table of precedent transactions, however, I do not have the time to compile such a list, and am running on experience at this point. My valuation for the second bid is posted below, with the valuation metrics underneath it.

Based on the metrics above, you can clearly tell that PAR was still undervalued after the initial bid. This would be even more clear based on table of precedent transactions, however, I do not have the time to compile such a list, and am running on experience at this point. My valuation for the second bid is posted below, with the valuation metrics underneath it.

- With exploreco's, it is difficult to put a value on the assets, as they are not operating or producing cash flow. You can value them using precedent transactions in the area based on a EV / acreage basis or on net risked resource potential, however, I do not have this information. Thankfully, the private placement financing puts a floor valuation of C$3.00 per share, which the market will no doubtly use in their risk-arb models.

- I value the warrant using a BS model, an assumed value of $3.00 for the exploreco stock, and exercise price of $3.00, an assumed expiry date of December 5th for the warrant, and a risk free rate of 2.25%. In addition, I assumed 40% volatility, which is what prop desks and hedge funds will use. In reality, this should be higher given that it is an exploreco. Also, I should note that management options have been priced using 55-65% volatility, which is reasonable, however, I am being conservative. With these assumptions, 1 warrant would be valued at ~C$0.25, and therefore 1/10th would equal C$0.025.

*NAV courtesy of PAR's June 2009 presentation. It is the average of analyst's estimates at the time.

Although, I personally think the second bid is still cheap as it is probably on the lower end of the valuation ranges, I would say that after two months of hard negotiations, this is about as good as it gets.

Just a side note on the exploreco valuation. The table below is from the presentation delivered upon the second deal announcement. As you can see, even analysts have no idea how to value the stub, as Peter's & Co puts a valuation of $0.40 on Trinidad and $1.05 on Colombia, whereas Raymond James is almost the complete opposite. In addition, they expect $1.40 of WC per share, whereas I expect the bought deal to be over-subscribed, and therefore this number should be around $1.75, leaving ~$1.25 in value for the Trinidad and Colombian assets.

HOW DO WE GET FROM A TO B?

The follow up question from all this analysis is this: Given all this information, how would you come to the conclusion that another deal was in the making? As an analyst, I would have answered your question as such:

- Takeover Bid Circular - The 55 page Circular was mailed literally the day after the hostile bid was announced. This almost never occurs, and as it is typically mailed about 2-4 weeks after announcement, depending on the complexity of the deal. This tells me that Pluspetrol had done its homework on PAR and was serious about buying the company very quickly.

- Extensions - Pluspetrol extended its Takeover Bid twice, which tells me that they were highly interested in acquiring PAR. This may also be indicative of negotiations going on in the background. This is especially true because such a complex structure emerged on September 3rd, which is one day after the second extension. I read that as both parties were negotiating long and hard in the background.

- Data Room - PAR opened its data room and confirmed that negotiations were occurring with interested parties. The increase in number of potential buyers is always good for a hostile deal as it opens up options for completing a deal.

- Valuation - At the initial bid, PAR was valued at ridiculously low price of $23,000 per boe/d and ~75% of NAV, with all the exploration assets included. I've never seen an O&G M&A valuation this low before. Although I do not have the resources to do a full analysis of precedent transactions, Highpine (HPX) was done at ~$37,000 per boe/d (which I thought was cheap as well). Some might point out that HPX produces light oil (68% light oil and ~$48 netbacks), whereas PAR produces heavy oil (100% heavy oil and ~$33 netbacks), however, a discount of that size was not warranted in my opinion.

- Operational Execution - Second quarter results were nothing short of amazing. Production was 14,403 boe/d, an uptick of 28% relative to 2008, while sales averaged 15,627 boe/d. Operating netback increased from $29.75 to $33.12 / boe. FFO was up 30% YoY, while net income increased 186% YoY. I should also note that PAR's was drilling at a 98% success rate so far this year. This information really shows that PAR is hitting on all cylinders and should be valued more like a producer than an explorer as time goes on. Read: It should be valued higher.

- Director's Circular - On page 21, the Director's Circular clearly states that Pluspetrol had previously offered $8.30 / share, obviously indicative that they thought the assets were worth more than $8.10. In addition, the circular mentions that they had examined spinning off assets as a potential course of action. I would have immediately done a back-of-the-envelope calculation of break-up value, although it would have been very difficult to get anything more than $1.75 per share given that the $3.00 financing had not been established until the second bid. In addition, there was no way to know that ALL the working capital of PAR would be transferred to exploreco. Hence, the worst case scenario is that you would assume ~$1.25 - $1.50 for the exploreco asset.

- Theory of Reflexivity - George Soros has written extensively about what he calls "The Theory of Reflexivity". The gist of the theory is that in a system, one part interacts with another in causing an effect, after which the 2nd part (which was just affected) causes a greater effect on the initial part. This interaction eventually spirals out of control in a constant loop. In PAR's case, the simple fact that the market consistently valued the shares about 11% above the initial deal price brings up the fact that no sane shareholder would have tendered the shares to the $8.10 bid if they could sell them in the market at ~$9.00 for weeks on end. This simple fact forced Pluspetrol to offer more than $9.00 to acquire PAR. The time delay also allowed PAR to develop more bidder and financing options, and also gave the advisors more than enough time to come up with a unique and viable break-up solution, which increased the value to shareholders even further. In my investing career, I have found that sometimes there is wisdom in crowds, and sometimes there is not. In the case of PAR, simply seeing that the stock was consistently being valued in the $9 range ($0.90 above the deal price) for weeks on end would prompt me to do further investigation as to why this was the case. The consistency and magnitude of the level of the stock price over and above the initial bid price would have screamed to me that there is greater value than what Pluspetrol was offering at the time. In hindsight, the market was obviously handicapping the probability of a deal being consummated because it would have valued the shares closer to $10.68 instead of the $9.43 it was being valued at prior to the announcement of the second deal, had investors believed in a higher deal price being realized.

- Incentives - PAR Directors & Officers owned ~11.1% of the FD shares outstanding. Not only did they hold real equity, but options with relatively low strike prices as well. In short, they were highly incentivized to find a higher bid. In addition, they had change of control payments in place, which further incentivized them to sell the company. This is in direct contrast to a company where management has no stake and may not be incentivized to do what is right for shareholders because it's interests are not aligned properly. They may, for example, be more interested in retaining their jobs or empire building.

So while it was impossible to know 100% that a higher bid was in the making, the signs were right in front of our eyes. Most people would say that hindsight is 20 / 20, and I agree completely. I also believe that with diligence and experience, it is possible to generate better outcomes. In my case, I am only tracking at about 25% of the "10,000 hour rule" in risk-arbitrage, but I know what to look for, and the more I practice, the better I seem to get. To me, getting a better handle on this deal than the market was a distinct possibility.

BASIC RISK-ARB ANALYSIS

The customary risk-arb analysis has been shortened, but I've included it below so that you get a further understanding of how the risk of this deal falling apart is almost nil.

- Regulatory Hurdles - None of significance. As Pluspetrol has been operating in Argentina for 32 years, I think the transfer of ownership is a mere formality. Exploreco will be the same as the structure is similar to the pre-deal PAR. No Canadian regulatory hurdles should be an issue, especially given that no PAR assets are located here, other than headquarters.

- Potential Timing Delays - The Management Information Circular is expected to be mailed by September 30th, with a shareholder vote date on October 30th. This is more than enough time given how long both sides have had to prepare.

- Bought Deal - I expect no issues with the bought deal. With 2 months of additional research by First Energy and Scotia Waterous, I believe they have not only a good handle on the geology / reserve / production potential of exploreco, but also the demand for shares. This is why they assumed the risk of a bought deal, and why I believe it will be over-subscribed. I also expect them to defend exploreco in the secondary market for the first month, which will net exploreco an additional $15mm in working capital. As the financing is expected to be completed on September 29th, a full 30 days before the shareholder vote, shareholders will find out how much WC exploreco will have before the deal even closes. If you look at how the press release is worded, exploreco will have money even before it is established as a corporate entity! They are basically assuming the deal will be done!

- Approval & Lock-ups - The Board of Directors approved the transaction based on the counsel of Scotia Waterous and First Energy Capital. Directors and Officers have agreed to vote in favour of the agreement. They represent roughly 11.1% of the FD shares. I should also note that Directors & Officers are basically taking profits on the producing assets and are buying into exploreco at C$3.00 - the exact same price that you can pay today by buying PAR on the open market. To me, this is a very good sign.

- Break Fees - Pluspetrol has agreed to pay PAR C$17mm should it back out of the deal. This is a normal fee, and is meant to compensate Pluspetrol for the time and resources it has spent on PAR should the deal not go through as planned. However, PAR has agreed to pay Pluspetrol a reverse break-fee of C$17mm should it back out of the deal. This is equivalent to ~C$0.34 / share, which is ~3% of the equity value of the deal. There are two things to mention here. First off, in my experience, reverse break-fees are rarely included in a deal, and are usually only included when that deal is expected to be final. Secondly, 3% of the equity value of the deal is expensive. The customary % is almost always around 2%, although it may be higher in this situation for the simple fact that both parties probably expended alot of corporate resources during the two month negotiations. Furthermore, it is important to note PAR does not need Pluspetrol to break-up the firm in order to realize value. The break-fee is almost solely attributable to the $7.65 portion for the Argentinean assets that are going to Pluspetrol, which means that the break-fee is actually 4.4% of the deal. In my experience, I've never seen a fee as large as that, and my translation is that it is in place to ensure that this deal gets done no matter what.

- Shareholder Vote - This is a non-issue. PAR shareholders should be ecstatic about what their management team has done for them. They also get management's value creation abilities in exploreco. In addition to the Director recommendation of acceptance as well as the lock-ups, shareholders would not want to irk the management team that has brought them so much success.

- Non-Solicitation & Right-To-Match Provisions - The deal includes both of these provisions, the first of which increases the certainty of the deal closing. The second one allows for further gains for shareholders should any other firm come to the table. They are both customary and good for the deal.

- Other Bids - At this stage of the game, there are no other bids. Bidders have had two months, and if PAR had any indication of a higher bid, they would not have gone to all the trouble of negotiating such a complex deal with Pluspetrol, nor would they have agreed to a reverse break-fee. However, if it happens while you are long PAR, then good on you.

- Spread & Annualized Return - At $10.40, PAR is yielding about 17% annualized based on my estimated deal close date of November 5th. Although I have not had a chance to look at the average or range of risk-arb spreads in Canada, my hunch is that this is about right, although you could see PAR rally a few pennies at the open on Tuesday. The dollar spread of $0.28 should slowly grind tighter, although hedge funds will not put on the spread in size for two reasons - 1) The deal has a long timeline of about 2 months. There is room to trade the spread around in that time, but you will see a few funds play it closer to the deal close. 2) There is no easy way to short exploreco or to hedge out the warrant. The C$7.65 value is a static value, however, the value of exploreco is really based on what investors perceive the value of the acreage and drilling potential to be. The C$3.00 value currently ascribed to the stub could easily be devalued should the bought deal not go swimmingly (leaving the dealers with large amounts of exploreco stock on their books, which will undoubtedly be an overhang on the stock), or if investors flee oil and gas exploration company stocks or international risk, thereby driving down the C$1.25 portion of the stub attributed to the land in Colombia and Trinidad & Tobago. As such, hedge funds will handicap the upside potential of exploreco until the deal is done. Given that the split up creates an exploreco and producing company, along with 1/10th of a warrant, what may actually happen on trading desks is the creation of a "grey market", whereby institutional investors that hold PAR will trade the unlisted shares and warrants of exploreco amongst each other, off the exchange. This is beneficial because it allows them to get access to the portion of the deal they like. Some investors may want to be long only the risk-arb spread (the producing assets), whereas others may want to be long only the exploreco, whereas other still may want to trade around the warrants based on volatility or acquire low volatility, short-dated warrants on the cheap if they can.

VALUE CREATION

So with the announcement of the second bid, I thought I would touch base on value creation. To be honest, this is one of the most astute examples of value creation I've ever seen in investing. It is literally a winning situation for each player involved.

- PAR shareholders - Received a 16.5% valuation bump with the initial bid, and a further 31.8% valuation bump from the second bid. Note that this could even increase further if the valuation of exploreco increases once it starts trading. In addition, the value of the warrants could further add to shareholder returns, albeit, very slightly.

- PAR management & directors - Walked away with a ~$15.2mm gain on their holdings from the pre-bid price (assuming the deal goes through). This does not include the gain on their option holdings, various change of control payments, any management contracts that Pluspetrol may offer them, or even the reputational gain that they've received for making shareholders so much money (only one financing is underwater).

- Pluspetrol Resources - Although it appears that they are paying ~$2.58 more than their original bid, I believe this new deal is actually better for them, and is more in line with what they were seeking. The company actually gets the producing resources it is seeking for $27,300 per boe/d. As PAR's Argentinean assets will exit 2009 at 20,000 boe/d, Pluspetrol is actually paying ~$20,500 per boe/d, which is ridiculously cheap relative to any transaction I've seen. And the truth is that at $8.10 per PAR share, Pluspetrol was getting the firm at $23,000 per flowing barrel, with ALL the exploration upside. This price was simply not realistic.

- First Energy Capital, Scotia Waterous / Capital - These two firms deserve to be recognized for proposing and negotiating an orderly break-up of PAR. For those unfamiliar with the mechanics of a break-up, sometimes the market values firms as 1 + 1 equals less than 2. A break-up seeks to alleviate this by maximizing value and changing that formula to 1 + 1 equals greater than 2. In this case, pre-bid PAR was a murky conglomeration of producing and exploration assets, seemingly straddling the line between both. By breaking up the assets into two separate entities, they could be more properly valued by the market as either producing or exploring. Save for the $0.025 1/10th warrant, there is absolutely no difference between a $8.10 bid for the whole PAR, and a $7.65 bid for the producing assets with the fully cashed-up exploration assets spun off at $3.00. Coming full circle, for these three advisors, the increase in reputation was worth the work alone in my opinion, however, they not only received M&A advisory fees of at least ~$4.6mm, but were also rewarded by becoming the syndicate for the bought deal for 5.3 - 6.6mm exploreco shares. The additional fees for this work will be on the order of ~$0.8 - $1.3mm in my estimation, and will be greater than a marketed deal as First Energy and Scotia Capital must put up their own capital and assume all the risk of selling the product. In short, this situation was a tremendous success for them.

THE REWARD

Let's assume that you spent a day after the initial Takeover Bid ($8.10) doing research, finally determined that the price of $8.10 was cheap, and therefore believed that a higher bid would be forth coming. Consequently, you bought shares at the close of that day ($9.15). Fast forward 78 days to September 4th, and your initial investment thesis comes to fruition, with Pluspetrol tabling a significantly higher offer which the market values at $10.40. Well, my friend, even though you assumed the risk of a deal not being completed and thereby potentially losing a good portion of your initial investment; you were rewarded handsomely for this risk by capturing a 13.8% return on your investment, which translates to a whopping 65% annualized return!

I should caution you that not all situations like this work out. The most painful hostile deal that comes to mind is when OMER's private equity arm, Borealis, engaged in a hostile Takeover Bid for Teranet Income Fund (TF.UN) at $11.00 / share, and then dropped the bid to $10.25 / share when no white-knights appeared. That was a personal investment dud for me, however, it taught me an important lesson about what I like to call "going with the flow". To me, it is imperative that you pay attention to the drivers of the underlying business of both the buyer and seller, as well as the financial markets, as changes in these factors can cause a change in how buyers and sellers perceive the value of the business, and hence, it can have an effect on the outcome of a deal. In the case of PAR, the strength in WTI (averaging around $70 / bbl) and other international E&P valuations from June through to August helped support the valuation of the stock. In essence, PAR had the benefit of the oil and stock markets on its side. Trust me when I say that Pluspetrol would have considered walking away if oil slipped to $50 / bbl. In the case of TF.UN, Borealis had the upper hand as the primary debt markets and therefore the M&A market dried up in the September to November period in 2008. With no financing available and commercial uncertainty running rampant, almost no firm could table a +$1.6bn offer for TF.UN. As such, Borealis took advantage by forcing a lower offer on unsuspecting shareholders. To my recollection, this outcome was not overly discounted in the stock, which is a realistic scenario for these situations.

So in closing, I will leave you with one final word on the topic of investing in hostile deals. I maintain that it is important to understand the probabilities in order to play the game properly - a 1997 analysis conducted by JP Morgan indicated that approximately 66% of all hostile deals end up being consummated, in one way or another (courtesy of "Deal, deals, and more deals...."). So, on that note, happy risk-arb investing, and I hope that all your deals turn out to be PARs....

Monday, August 31, 2009

The SEC Should Ban High Frequency Trading

The discussion in the past few months regarding “High Frequency Trading” has been deep and persistent, especially given the SEC’s recent initiation of a review of the strategy on Wall Street. This success and importance of this little-known strategy has also been highlighted in recent months by Goldman Sach's $4bn profit in Q2 (driven in part by HFT), as well as the theft of Goldman’s proprietary high frequency trading strategy by a former employee

For those who are unaware of this strategy, high frequency trading is basically an algorithm that allows incredibly fast access to various markets by traders (think millionths of a second). Flash trading also allows a trader to “flash” orders on an exchange for a fraction of a second, oftentimes ahead of other orders in the queue. The issue here is that there are potential abuses that could occur because of this strategy – abuses that can undermine confidence in and stability of the market.

Arguments have been made that you cannot regulate the progress of trading strategies and technologies just because some market participants are superior traders or have better access to technology. I agree that this type of regulation is impractical and goes against free market principles. However, supporting high frequency trading ignores the 2nd (and higher) order effects of this decision, which, net-net, are more important to the overall stability of and confidence in the fairness of the markets than the profits of a select group of trading firms. First off, I should clarify that I do not take issue with the “speed” factor of the algorithms. As almost every exchange has moved away from an "open outcry" trading system towards an electronic system, speed and the cost efficiency of trading have improved several fold in the last few decades, and will most likely continue to do so. Simply put, this is positive for all investors. Nor do I take issue with the “frequency” factor. The frequency of trading is in essence, liquidity, which is positive for both sellers and buyers. What I do take issue with is the fact that these flash orders can potentially allow traders to get a “free look” by trading on different exchanges than they should normally be trading on (should they not have had the possibility to execute flash orders). This type of technology can also potentially be used to manipulate the price of a security in favour of the trader. These factors alone should be enough to convince you that high frequency trading is dangerous.

However, the typical rebuttal from high frequency traders is that anyone with enough capital can purchase the requisite technology and expertise needed to employ this strategy, hence there is no unfair advantage to anyone using it. While this is true, the practical reality is that a very select few trading firms (select hedge funds / prop desks) have the ability to implement and execute high frequency trading strategies. These firms are privileged enough as it is, and do not need the additional advantage of having the ability to front-run their clients or trade ahead of the market, regardless of whether or not they will actually do so. Allowing high frequency trades and flash trades is irresponsible because while it does not promote front-running, it does allow the potential for it. We should protect the markets against any threat of manipulation, because in my experience, any advantages (fair or unfair) will be used on The Street. Unless the SEC can regulate AND effectively enforce any market abuses resulting from high frequency flash trading, it should be banned. History has shown that the SEC has not only been consistently behind the curve in recognizing market abuses (for a recent example, see the SEC announcing a review of Goldman's trading huddle practices literally the day after they were detailed on the front page of the WSJ), but has been almost wholly ineffective at halting various frauds and scams. This is why, in my view, high frequency trading should be curtailed now before it becomes the next big scandal on Wall Street.

For those who are unaware of this strategy, high frequency trading is basically an algorithm that allows incredibly fast access to various markets by traders (think millionths of a second). Flash trading also allows a trader to “flash” orders on an exchange for a fraction of a second, oftentimes ahead of other orders in the queue. The issue here is that there are potential abuses that could occur because of this strategy – abuses that can undermine confidence in and stability of the market.

Arguments have been made that you cannot regulate the progress of trading strategies and technologies just because some market participants are superior traders or have better access to technology. I agree that this type of regulation is impractical and goes against free market principles. However, supporting high frequency trading ignores the 2nd (and higher) order effects of this decision, which, net-net, are more important to the overall stability of and confidence in the fairness of the markets than the profits of a select group of trading firms. First off, I should clarify that I do not take issue with the “speed” factor of the algorithms. As almost every exchange has moved away from an "open outcry" trading system towards an electronic system, speed and the cost efficiency of trading have improved several fold in the last few decades, and will most likely continue to do so. Simply put, this is positive for all investors. Nor do I take issue with the “frequency” factor. The frequency of trading is in essence, liquidity, which is positive for both sellers and buyers. What I do take issue with is the fact that these flash orders can potentially allow traders to get a “free look” by trading on different exchanges than they should normally be trading on (should they not have had the possibility to execute flash orders). This type of technology can also potentially be used to manipulate the price of a security in favour of the trader. These factors alone should be enough to convince you that high frequency trading is dangerous.

However, the typical rebuttal from high frequency traders is that anyone with enough capital can purchase the requisite technology and expertise needed to employ this strategy, hence there is no unfair advantage to anyone using it. While this is true, the practical reality is that a very select few trading firms (select hedge funds / prop desks) have the ability to implement and execute high frequency trading strategies. These firms are privileged enough as it is, and do not need the additional advantage of having the ability to front-run their clients or trade ahead of the market, regardless of whether or not they will actually do so. Allowing high frequency trades and flash trades is irresponsible because while it does not promote front-running, it does allow the potential for it. We should protect the markets against any threat of manipulation, because in my experience, any advantages (fair or unfair) will be used on The Street. Unless the SEC can regulate AND effectively enforce any market abuses resulting from high frequency flash trading, it should be banned. History has shown that the SEC has not only been consistently behind the curve in recognizing market abuses (for a recent example, see the SEC announcing a review of Goldman's trading huddle practices literally the day after they were detailed on the front page of the WSJ), but has been almost wholly ineffective at halting various frauds and scams. This is why, in my view, high frequency trading should be curtailed now before it becomes the next big scandal on Wall Street.

Monday, August 17, 2009

Blodget & Spitzer...Round 2

I wanted to post this fantastic interview delivered by Henry Blodget, who sits down with the former New York State Attorney General, Eliot Spitzer, to discuss AIG, the bailouts, compensation, and regulatory roles. I have always maintained that Eliot Spitzer was one of the shrewdest regulators of our time because he almost single-handedly took on Wall Street in reigning in illegal acts by many of the largest investment banks throughout his tenure.

http://www.thedeal.com/dealscape/2009/08/henry_blodget.php

What I find particularly interesting about this interview is Spitzer's clarity on the issues that have plagued Wall Street over the past 2 years. He calls out the government's failed involvement in the bailout of AIG, how regulators have enough power as it is, as well as how regulators and the regulatory system have failed to an extent. His rationale on each of these issues is second to none, and it is a shame that he is not in the same position of power that he once was. If there ever was a time that Main Street needed Eliot Spitzer to protect it from Wall Street, it would be now. While I am generally an advocate of the free market economy, Spitzer's "no-holds-barred" approach to regulation is just the tonic our society needs to better deal with the ongoing corporate malfeasance. As Spitzer himself said, the drive for wealth creation is inherently good for society; however, it is the after effects of that insatiable drive that we must avoid, as it's damage is greater than the benefits of being a purely free market.

http://www.thedeal.com/dealscape/2009/08/henry_blodget.php

What I find particularly interesting about this interview is Spitzer's clarity on the issues that have plagued Wall Street over the past 2 years. He calls out the government's failed involvement in the bailout of AIG, how regulators have enough power as it is, as well as how regulators and the regulatory system have failed to an extent. His rationale on each of these issues is second to none, and it is a shame that he is not in the same position of power that he once was. If there ever was a time that Main Street needed Eliot Spitzer to protect it from Wall Street, it would be now. While I am generally an advocate of the free market economy, Spitzer's "no-holds-barred" approach to regulation is just the tonic our society needs to better deal with the ongoing corporate malfeasance. As Spitzer himself said, the drive for wealth creation is inherently good for society; however, it is the after effects of that insatiable drive that we must avoid, as it's damage is greater than the benefits of being a purely free market.

Tuesday, July 28, 2009

Thoughts on the SEC's short sale actions

Short selling has been on the receiving end of public scrutiny and outrage for the past few quarters, as many believe hedge funds are to blame for the financial crisis. While hedge funds may have added fuel to the fire, their use of short selling did not cause the problems we are experiencing today. In my view, short selling is extremely useful because it allows market participants more ways to express their views on the value of a security, and thereby profit. It also acts as a counter-balance against the undue optimism sometimes present in a security, and can bring that security's price back to reality.

Whether you are for or against short selling, I think all of us can agree that the SEC's monitoring and regulation of short selling, and in particular naked short selling, has been poor at best. Just to clarify, naked short selling is the act of short selling when you do not have the "borrow" available. It is a particularly pernicious activity because it can allow someone to manipulate the market for a security.

Yesterday, the SEC announced several measures designed to better regulate and disclose the act of short selling (http://www.sec.gov/news/press/2009/2009-172.htm).

The measures are three-fold:

Whether you are for or against short selling, I think all of us can agree that the SEC's monitoring and regulation of short selling, and in particular naked short selling, has been poor at best. Just to clarify, naked short selling is the act of short selling when you do not have the "borrow" available. It is a particularly pernicious activity because it can allow someone to manipulate the market for a security.

Yesterday, the SEC announced several measures designed to better regulate and disclose the act of short selling (http://www.sec.gov/news/press/2009/2009-172.htm).

The measures are three-fold:

- Brokers must purchase or borrow securities to deliver on a short sale. While this rule was already in place, it is being made permanent in order to curtail naked short sales.

- A plan for SRO's to publicly disclose price and volume information regarding short sales. They are also continuing to review proposals on short sale price tests and circuit breakers for individual stocks.

- A roundtable will be held on September 30th to discuss new measures including "securities lending, pre-borrowing, possible additional short sale disclosures, the potential impact of a program requiring short sellers to pre-borrow their securities, possibly on a pilot basis, and adding a short sale indicator to the tapes to which transactions are reported for exchange-listed securities".

I believe these measures are extremely positive for the market. I do applaud the SEC's efforts in (hopefully) regulating short sales the way they should be regulated, and increasing short sale transparency through more public disclosure. The only real negative to come from all of this is that all of this new regulation requires resources - resources that could be put to better use. In particular, it will increase the costs involved for short sellers - most likely legal and compliance.

Saturday, July 25, 2009

Societal Implications Of The Market Collapse

As I am MBA bound in mid-August, I thought it was a good idea to present Bloomberg's recent article (http://www.bloomberg.com/apps/news?pid=20601109&sid=aQn_Cxyu99xY) on how the market rout of the past two years has affected Universities throughout the world. Most University endowments lost 20-30% from their peaks in (roughly) June 2008, and I believe the results achieved by the endowments will have prolonged effects on North America. It is well documented that we are past the industrial revolution and that we are well into the technological revolution. For North America to continue its lead on the world stage, we must continue to grow our technological lead, because this is where the future lies. At its most basic level, future growth will come from investment in the educational infrastructure of our society. These investments are designed to help spur innovation, eventually leading to impactful changes on our society (scientific, commercial, etc). Simply put, this is a requirement for the success of our society.

As pointed out in the article, many of our higher educational institutions that produce these breakthroughs have been forced to cut back on funding - postponement of the construction of buildings, lowering of professor salaries, halting program expansions, shrinking programs and research projects, etc. Furthermore, these cuts will be long-lived, because Universities generally derive a large chunk of their funding from endowments. However, to protect from outlier year's returns affecting funding, universities generally smooth the asset values of their endowments over three years to attain an average from which to draw a percentage of said funds for spending purposes. While this approach works the majority of the time, a problem really arises in times of distress where the endowment suffers multiple down years. Universities have already cut back on spending to compensate for an inevitable decline in their income stream; however, this decline will almost certainly be semi-permanent in nature. In fact, the larger and more prominent endowments are predicting that they will not be able to achieve their peak endowment size for anywhere from ten to fifteen years. To me, this means restricted growth in University funding, which may translate into slower long-term growth in our society - something that we cannot allow to happen.

While few organizations saw the market correction coming, I believe most endowment's investment strategies have actually aggravated their losses in this downturn. To understand how this occurred, you must understand that endowments were founded on the Prudent Man Rule, which basically states that they must manage their assets as a "prudent man" would, focusing on capital preservation primarily, followed by the earning of a respectable return. By that definition, most endowments have failed miserably over the past two years. As the purpose of an endowment is to fund long-duration liabilities (the maintenance and growth of the income stream of a University into perpetuity), the natural thing to do is to match those liabilities with long-duration assets. The first iteration of endowment investment strategy involved their assets being invested in long-term government bonds and high-quality corporate credits. This continued until equities started becoming a viable institutional asset class (again) in the 1950's and 1960's. During that time-period, Modern Portfolio Theory was created which was then incorporated in the endowment world - most famously by David Swensen, Yale's endowment manager. Swensen pioneered the use of MPT in endowment asset management starting in 1985, and focused on diversification as a way of achieving higher alpha. However, he did not simply diversify based on credit rating or sector. Swensen diversified into unconventional and uncorrelated asset classes such as hedge funds, real estate, venture capital, private equity, commodities, and timberland. Yale's endowment benefited handsomely from this approach to asset management for years, generating double-digit returns (http://www.yale.edu/investments/Yale_Endowment_08.pdf) which other endowments envied and eventually imitated. Although, this approach was like a double-edged sword, as the common link amongst all those investment asset classes is that they are illiquid and have high frictional costs. For example, hedge funds often have lock-up periods of two or more years. Private equity funds have lock-up periods of 7 to 10 years. Real estate and timberland can be notoriously illiquid, especially at the wrong time and price. Endowments embraced these asset classes and increased their portfolio weightings throughout the 1990's and 2000's. The additional alpha generated from investing in unloved and uncovered areas helped produce +15% returns for most endowments over this period. However, when the liquidity-seeking panic selling began in mid-to-late 2008, endowments were caught offside, losing billions in the process. These funds are not nimble and cannot turn their strategies on a dime. Their actions affect the market because, in essence, they are the market, and this is especially true when you consider that the size of the market for these strategies can be small. They are also inefficient, resource intensive, volatile, hard to enter and exit, and expensive to enter and exit. Furthermore, as the Bloomberg article pointed out, these areas have been slow to rebound, and it is very difficult to say whether or not they will reach the level of popularity they achieve pre-credit crisis. Some of these endowments are now stuck in these illiquid investments, and have been forced to raise cash for funding requirements via debt issues (Harvard issued $2.5bn in debt in 2008). In short, the acceptance of illiquidity has now caused long-term structural issues in terms of asset and liability matching. These funds, supposedly conservative in nature, are having a difficult time meeting their mandates - providing stable streams of income to match their Universities funding requirements.

As they say, hindsight is 20-20, which is why I believe it is actually hard to fault these managers for pursuing such strategies. The investment world is complex and competitive. These managers had the proverbial gun to their heads and were involved in a dual - the pursuit of the highest alpha. The truth is that if they did not pull the trigger in employing these alpha-seeking strategies, somebody would come along and pull the trigger at their expense. Furthermore, it is hard to fault them for being unable to change what has worked for so long. As humans, we are susceptible to hindsight bias. Seeing a competing manager consistently earn +15% returns with low volatility for years will often fool us into believing that that strategy is sustainable. This is clearly not always the case, and certainly brings into question the wisdom of maintaining an investment policy of effectively static portfolio weightings in asset classes over the long-term.

It makes one wonder whether straying from the essence of the Prudent Man Rule was so wise? Does the pursuit of return trump the pursuit of capital preservation? Although my investing career has been relatively short, the longer I am in this game, the more I think that capital preservation is the essence of investing. Wealth accumulation is, after all, path dependent. Simple arithmetic tells us that losing X% requires us to produce a return greater that X% for us to simply get back to even, and more importantly, it robs us of the time (read: opportunity cost) that our funds could be employed in an investment producing positive returns.

Tuesday, July 21, 2009

Opportunity Costs Really Grind My Gears...

Do you want to know what really grinds my gears? Opportunity costs. That moment we have all experienced - when a stock that has been on your watch list for the past year suddenly receives an offer to be acquired or jumps +20% in a day. That moment when you realize that all that work you did in the interim seemingly goes down the tubes because you can no longer act on your research at an attractive price. For me, that moment has been replayed over and over in the past five months, as so many of the stocks that I wish I had bought have doubled and / or tripled. The last stock to contribute to the continued crushing of my spirit was Cossette Communications Group (TSX: KOS), a stock that I have been following for quite a while. It has been in a downward spiral for years, and I have been watching it fall further and further, knowing that one day its fortunes would rebound. Aside from the cheap valuation which initially attracted me, I saw KOS as a company with several corporate governance issues (dual class share structure, insider dealings, and board independence issues specifically) and a business under temporary pressure given its economically sensitive revenue streams. If the corporate governance issues could be fixed and advertising spending stabilized, I believed that we could easily see the stock in the high single-digits. While none of that has played out, the day of reckoning came yesterday, as the company received an unsolicited proposal to be acquired by Cosmos Capital by way of Takeover Bid for C$4.95 per subordinate voting share - a 52% premium over the previous day's closing price.

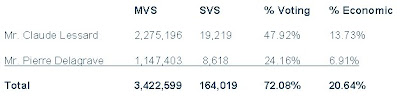

Cosmos Capital is an entity controlled by Mr. François Duffar, a former director of KOS, who resigned effective June 1st, 2009. Other investors include George Morin, Jean Monty, Daniel Bernard, and an un-named multi-billion dollar private equity group. Mr. George Morin, another KOS director, officially tendered his resignation as of July 18th, which just became known yesterday by way of a KOS press release. Together with Mr. Claude Lessard and Mr. Pierre Delagrave, the four members of the Board held all of the multiple voting shares, which essentially gave them an 85.9% voting interest in the firm, but only 37.9% economic ownership. However, once Duffar and Morin left the board, their MVS were automatically converted into SVS, leaving the main ownership structure as follows:

Now, with Duffar and Morin owning 3.1mm SVS, their voting interest is 6.5%, but their economic interest is 18.6%, which represents the second largest block of shares after Lessard and Delagrave (assuming they are aggregated). On a side note, Burgundy Asset Management owns 1.9mm SVS, representing a 3.99% voting interest and 11.37% economic ownership.

Now this is interesting, as you can see a power struggle emerging between four colleagues who have (had) high positions in management and on the board, and who essentially control the firm via their MVS. Given that the stock has traded at the C$4.95 Takeover Bid price on announcement day (and in fact traded at C$5.15 to close the day) shows that the market and specifically merger-arbitrage players believe that there is more upside to this story. In fact, today, the stock traded mostly above C$5.00, and closed at C$5.20, albeit on small volume (72,000 shares traded). This may indicate that speculative retail players are buying up here. I would expect higher volume created from arbitrageurs buying below the C$4.95 level.

The truth is that it does not take a genius to figure out that Cosmos Capital is trying to pick up the company on the cheap, as one only has to take a cursory look at the facts to see this (http://www.cossette.com/investors/pdf/inv_Factsheet_KOS_20090506.pdf). Looking at EV / normalized EBITDA shows that Cosmos Capital is proposing to pay ~3x. If you factor in cap-ex to get a basic FCF, we are looking at 3 to 4x EV / FCF, which is still extremely cheap. It is reasonable to assume that the range of EPS in a normalized operating environment is anywhere from $0.50 to $0.90, which implies that Cosmos is attempting to pay anywhere from 5.5x to 9.9x earnings, which despite the high premium on 30 day VWAP and previous day closing price, is not much of a valuation premium. While not entirely comparable due to size and geographic diversity, the comps (Interpublic, WPP, and Omnicom) are trading at 11 to 12x trailing EPS. It is also important to keep in mind that these are bottom cycle EPS numbers as well, so there is certainly room for upside for any acquiror. Aside from these basic valuation measures, the best information to look at in this situation would be media (specifically advertising company) acquisition premiums and valuation metrics, however I am not a media analyst, so I do not have enough historic information to do a proper analysis. My gut instinct and the information I do have tells me that this proposal is inadequate, and we will see the newly formed special committee either force a higher bid from Cosmos or another party (likely Lessard) via an auction process.

While I do believe a higher bid will be forthcoming, there are a few caveats for anybody wishing to play this from a merger-arbitrage perspective. First off, this is only a proposed Takeover-Bid, which means this is a risk because no deal is actually on the table as of yet. In addition, because Cosmos Capital technically already owns an 18.7% position in the stock, you must be aware that they have already benefited from the jump in the stock price, and this is before anything other than the proposal has occurred. Therefore, they may have ulterior motives and it wise to be aware of that possibility. Secondly, Burgundy Asset Management owns an 11.1% economic interest in the firm, and Cosmos has convinced them to sign a "hard lock-up" agreement, meaning that they cannot sell their shares below the C$4.95 bid, unless a higher bid is tabled. This is important because it means that 30% of the shares, yet only 10.4% of the votes, are in favor of the deal from the get-go. Although I have never been in favour of the dual class share structure, this is exactly why it was created, as Lessard and Delagrave now have an extremely valuable blocking position. Finally, my biggest hesitation in playing this deal is that I do not have a read on what Lessard is thinking. He is the largest shareholder, and he was clearly kept out of Cosmos Capital's bid, which may have irritated him and may cause him to reject their bid outright. This is important because he controls a 47.4% voting interest in the company, and therefore can block any proposal he wants. (66 2/3% is the generally the required amount for a Takeover Bid to close). It is also important to note that the firm is essentially his baby, as he started his career at KOS in 1972 as President & CEO, and has built it into what it is today. So, does he actually want to sell the firm now and at the price Cosmos is offering? Also, does he want to sell to ex-colleague's that went behind his back with a Takeover Bid in an attempt to "steal" his company from him? My guess is no. He is also the most incentivized person in terms of seeing a higher stock price, so my guess is that he will 1) have the special committee search for a higher bid (this is obvious) or 2) emerge as a bidder himself. From 1996 to 2008 he has received salary and bonus compensation of anywhere from $600,000 to $1,000,000 per annum, and as he has held his same position since 1972, he likely had a similar compensation scheme from 1972 to 1996 (adjusted for inflation). My point is that he is likely wealthy enough to arrange his own bid in some way, shape, or form.

Regardless of the risks to this proposal, I am still positive on a deal materializing, however, at the +C$5.00 level, buying shares now leaves no room for error. Given that KOS is now a risk-arb situation as opposed to just a cheap stock, the risk / return parameters have changed. As such, I would remain on the sidelines until this becomes an official bid, and until you have a chance to read the Takeover Bid circular. In addition, I would be a buyer at a positive spread - likely at the C$4.75 level. This is equivalent to a 21% annualized return according to my deal timeline assumptions, and it takes into account the risk of Lessard using the "just say no" defense. Unfortunately, it does not look like KOS is going to get to that level anytime soon.

So, to circle back to the beginning of this post, the best thing we can do is learn from our mistakes and move on. So the question becomes what did I learn from this missed opportunity?

My take-aways are three-fold:

Cosmos Capital is an entity controlled by Mr. François Duffar, a former director of KOS, who resigned effective June 1st, 2009. Other investors include George Morin, Jean Monty, Daniel Bernard, and an un-named multi-billion dollar private equity group. Mr. George Morin, another KOS director, officially tendered his resignation as of July 18th, which just became known yesterday by way of a KOS press release. Together with Mr. Claude Lessard and Mr. Pierre Delagrave, the four members of the Board held all of the multiple voting shares, which essentially gave them an 85.9% voting interest in the firm, but only 37.9% economic ownership. However, once Duffar and Morin left the board, their MVS were automatically converted into SVS, leaving the main ownership structure as follows:

Now, with Duffar and Morin owning 3.1mm SVS, their voting interest is 6.5%, but their economic interest is 18.6%, which represents the second largest block of shares after Lessard and Delagrave (assuming they are aggregated). On a side note, Burgundy Asset Management owns 1.9mm SVS, representing a 3.99% voting interest and 11.37% economic ownership.

Now this is interesting, as you can see a power struggle emerging between four colleagues who have (had) high positions in management and on the board, and who essentially control the firm via their MVS. Given that the stock has traded at the C$4.95 Takeover Bid price on announcement day (and in fact traded at C$5.15 to close the day) shows that the market and specifically merger-arbitrage players believe that there is more upside to this story. In fact, today, the stock traded mostly above C$5.00, and closed at C$5.20, albeit on small volume (72,000 shares traded). This may indicate that speculative retail players are buying up here. I would expect higher volume created from arbitrageurs buying below the C$4.95 level.

The truth is that it does not take a genius to figure out that Cosmos Capital is trying to pick up the company on the cheap, as one only has to take a cursory look at the facts to see this (http://www.cossette.com/investors/pdf/inv_Factsheet_KOS_20090506.pdf). Looking at EV / normalized EBITDA shows that Cosmos Capital is proposing to pay ~3x. If you factor in cap-ex to get a basic FCF, we are looking at 3 to 4x EV / FCF, which is still extremely cheap. It is reasonable to assume that the range of EPS in a normalized operating environment is anywhere from $0.50 to $0.90, which implies that Cosmos is attempting to pay anywhere from 5.5x to 9.9x earnings, which despite the high premium on 30 day VWAP and previous day closing price, is not much of a valuation premium. While not entirely comparable due to size and geographic diversity, the comps (Interpublic, WPP, and Omnicom) are trading at 11 to 12x trailing EPS. It is also important to keep in mind that these are bottom cycle EPS numbers as well, so there is certainly room for upside for any acquiror. Aside from these basic valuation measures, the best information to look at in this situation would be media (specifically advertising company) acquisition premiums and valuation metrics, however I am not a media analyst, so I do not have enough historic information to do a proper analysis. My gut instinct and the information I do have tells me that this proposal is inadequate, and we will see the newly formed special committee either force a higher bid from Cosmos or another party (likely Lessard) via an auction process.

While I do believe a higher bid will be forthcoming, there are a few caveats for anybody wishing to play this from a merger-arbitrage perspective. First off, this is only a proposed Takeover-Bid, which means this is a risk because no deal is actually on the table as of yet. In addition, because Cosmos Capital technically already owns an 18.7% position in the stock, you must be aware that they have already benefited from the jump in the stock price, and this is before anything other than the proposal has occurred. Therefore, they may have ulterior motives and it wise to be aware of that possibility. Secondly, Burgundy Asset Management owns an 11.1% economic interest in the firm, and Cosmos has convinced them to sign a "hard lock-up" agreement, meaning that they cannot sell their shares below the C$4.95 bid, unless a higher bid is tabled. This is important because it means that 30% of the shares, yet only 10.4% of the votes, are in favor of the deal from the get-go. Although I have never been in favour of the dual class share structure, this is exactly why it was created, as Lessard and Delagrave now have an extremely valuable blocking position. Finally, my biggest hesitation in playing this deal is that I do not have a read on what Lessard is thinking. He is the largest shareholder, and he was clearly kept out of Cosmos Capital's bid, which may have irritated him and may cause him to reject their bid outright. This is important because he controls a 47.4% voting interest in the company, and therefore can block any proposal he wants. (66 2/3% is the generally the required amount for a Takeover Bid to close). It is also important to note that the firm is essentially his baby, as he started his career at KOS in 1972 as President & CEO, and has built it into what it is today. So, does he actually want to sell the firm now and at the price Cosmos is offering? Also, does he want to sell to ex-colleague's that went behind his back with a Takeover Bid in an attempt to "steal" his company from him? My guess is no. He is also the most incentivized person in terms of seeing a higher stock price, so my guess is that he will 1) have the special committee search for a higher bid (this is obvious) or 2) emerge as a bidder himself. From 1996 to 2008 he has received salary and bonus compensation of anywhere from $600,000 to $1,000,000 per annum, and as he has held his same position since 1972, he likely had a similar compensation scheme from 1972 to 1996 (adjusted for inflation). My point is that he is likely wealthy enough to arrange his own bid in some way, shape, or form.

Regardless of the risks to this proposal, I am still positive on a deal materializing, however, at the +C$5.00 level, buying shares now leaves no room for error. Given that KOS is now a risk-arb situation as opposed to just a cheap stock, the risk / return parameters have changed. As such, I would remain on the sidelines until this becomes an official bid, and until you have a chance to read the Takeover Bid circular. In addition, I would be a buyer at a positive spread - likely at the C$4.75 level. This is equivalent to a 21% annualized return according to my deal timeline assumptions, and it takes into account the risk of Lessard using the "just say no" defense. Unfortunately, it does not look like KOS is going to get to that level anytime soon.

So, to circle back to the beginning of this post, the best thing we can do is learn from our mistakes and move on. So the question becomes what did I learn from this missed opportunity?

My take-aways are three-fold:

- When you do your homework, you must believe in your analysis, and must be ready to pull the trigger when an opportunity comes your way.

- The sense of loss I felt upon finding out about the Takeover Bid for KOS was natural. It is only human nature to feel remorse over a potential gain when I had the desire and ability to buy KOS, but did not. It is also natural that this feeling is stronger than an actual monetary loss on a stock, because as humans, we feel that once we have made the decision to buy, the "fate" of the stock is now out of our control, and therefore we attribute this loss to the markets and not ourselves. Conversely, it is interesting that should that stock have gone up after our purchase, the majority of us would attribute it to our savvy investment skills, and not the stock's "fate". Regardless, these feelings are behavioral in nature, and we have to learn to combat them because they can and will lead to mistakes.

- The physical matters. By this, I mean it is vitally important that as analysts, we look through the DCFs and EPS and all the other investment jargon. We have to look at the tangible aspects of a business, because sometimes there are physical clues that sit right in front of our eyes. With respect to KOS, this clue emerged on March 2nd, 2009 when KOS issued a press release announcing that Mr. Francois Duffar, the Vice-Chairman of the Board of Directors and a member of the management team of KOS since 1972, decided to terminate his employment with the firm as of June 1st. While management turnover is normal (especially for someone who has had a 37 year career with the same firm), it is the fact that this action caused his MVS to be automatically converted to SVS. This is what should have tipped me off that something was in the works. In my view, no rational person would willingly give up the control premium that typically comes with MVS, and certainly not without getting something in return. On May 11th, it was announced that Duffar would step down from the Board of Directors, effective that day. This was another hint that I should have picked up on instantly. Fast-forward 70 days, and the stock is up 65.5%, which on Duffar's 2.09mm SVS, represents a paper gain of C$4.1mm, and in my view, the recouping of the control premium he rightfully possessed on his MVS. The physical matters...

Saturday, July 18, 2009

Life in the M&A deal market?

Thomson Reuters recently released first-half 2009 M&A deal statistics, which seems to indicate that we have, in fact, turned the corner in the M&A market. At the very least, activity is picking up in terms of small and mid-market deals.

As indicated in the Thomson Reuters blog (below), first half deals are down 45.7% in dollar terms YoY. However, while second quarter mid-market deals were down 43% YoY in dollar terms, they came in 20% ahead of the first quarter, which is stability at the very least.

http://blogs.reuters.com/reuters-dealzone/2009/07/13/keeping-score-signs-of-life-in-the-mid-market/

As I have maintained throughout downturn, small and mid-market deals are where we will see strength first, as large-cap and mega-cap deals require huge amounts of financing, which requires significant primary debt market demand - something that is not fully back.

Although this information is definitely positive, it does remain to be seen whether or not this is the end of the pain in the deal market, as there are various views on whether or not we are fully out of the woods yet. The consensus amongst M&A professionals, as per a recent WSJ DealJournal blog post (below), is a firm no.

http://blogs.wsj.com/deals/2009/07/10/ready-to-call-bottom-in-the-ma-market/

Thursday, July 16, 2009

1st Half 2009 Hedge Fund Returns

Courtesy of Credit Suisse / Tremont Hedge Index (http://www.hedgeindex.com/)

As we are now a little past half way through the year, I believe it is important to take a quick glimpse at how the markets are doing. Overall, the S&P 500 is up ~1.7%, the DJIA is down ~3%, and the NASDAQ is up ~14%. Mixed results, overall, but it is a welcomed trend given the destruction that occurred last year. Markets have also been buoyed over the past few days due to the much anticipated Goldman Sachs and Intel results - both of which came in above expectations earlier this week.

While the overall markets have remained flat (albeit, with significant volatility), hedge fund strategy returns have been extremely mixed. As I had predicted earlier this year, convertible arbitrage would come back strongly after the debt market was flooded with primary market issuance earlier this year. Convertible arbitrage is up an astounding 24% YTD, as credit markets continued to heal, while opportunities for shorting equities were abundant in the earlier part of this year. Given the massive rallies in all equities since the March lows, I am not surprised that dedicated short funds were down an average of 10% as well. What is an aberration, however, is the fact that equity market neutral funds are down an astounding 14% YTD.

Looking forward in the mid-term (+1 year), I do see three strategies doing well. First off, Global Macro should continue to do well, as there is still significant volatility in essentially all asset classes, and there will continue to be as long as there is the perception of risk in the markets and as long as world-wide governments, central banks, and various regulatory agencies continues to interfere in natural market mechanisms. One simply has to look at what has gone on in base metals, precious metals, energy commodities, equities, distressed debt, real estate, currencies, interest rates, etc. This playing field is a bonanza for Global Macro managers as they have access to essentially every asset class that is displaying huge, albeit, declining volatility.

Secondly, I expect Long / Short Equity managers to do well in this environment, because I do expect the VIX to be quite active in the near future, albeit in a trading range of 20 - 40 (it is currently at 26). Note that I view the VIX as the market's perception of current risk, and not future risk. With every market participant's heightened sense of risk and this economic crisis continuing, we are definitely not going back to below 20 on the VIX anytime in the near future. With Long / Short managers finally starting to catch their bearings after last years market rout, directional short-term trading and stock picking will be the main source of returns in the near future. Assuming most Long / Short managers have the wherewithal to stomach volatility and take advantage of short-term market swings, I do see this strategy performing as it has always been marketed to perform.

Finally, Event-Driven / Distressed Debt funds will also benefit in the coming years. Although M&A deal volumes and values are hitting all-time lows, it is only a matter of time before this market turns the corner and deals starts hitting the tape again. Risk-Arbitrage will be back when the deal market and hedge funds stabilize. Note that this is also dependent on the securities lending market and prime brokerage financing stabilizing as well. A separate, yet related strategy is the Distressed Debt strategy, and I strongly believe that we will see that come back as corporate bankruptcies (14,319 in the 1st quarter of 2009 - a number we have not seen since www.abi.org began recording in 1994) and restructurings continue to proliferate. We have already seen major funds flow into the sector, along with new restructuring funds being opened up. This type of activity will only increase, and therefore I do see numerous opportunities in this sector. However, these workouts will take time, and therefore returns will take longer to achieve.

Tuesday, July 7, 2009

New Venture Capital Fund - Andreessen Horowitz

Yesterday, Marc Andreessen, the founder of Netscape, announced the formation of a new VC firm called Andreessen Horowitz, with his partner Ben Horowitz. Andreessen has also been involved in Facebook, Twitter, and NetScape. This new tech focused fund is unique in that it has limited its scope to tech investments solely based in America. The $300mm fund will also focus on investments ranging in size from $50,000 up to $50mm.

http://dealbook.blogs.nytimes.com/2009/07/06/netscape-founder-starts-silicon-valley-venture-firm/