On December 15th, Novartis announced that it had come to terms with the Board of Directors of Alcon, and proposed a deal to acquire the remaining 23% stake in Alcon it did not already own from minority shareholders (http://invest.alconinc.com/phoenix.zhtml?c=130946&p=irol-pressReleasesArticle&ID=1507867&highlight=). The reason why this is important is because the history of the deal extends for several years, and Novartis initially attempted to squeeze out minority shareholders for significantly less consideration than it paid for the controlling stake it acquired in Alcon from Nestle. This was a significant win for minority shareholders, as Novartis had no such obligation to give them as much consideration as Nestle under Swiss securities law. Here is a brief outline of what occurred:

• April 7th, 2008 - Novartis acquired a 25% stake in Alcon from Nestle for $143.18 in cash consideration. The deal had some interesting provisions worked in, whereby Novartis had the option to acquire Nestle's remaining 52% stake by a certain date at a certain price.

• January 4th, 2010 - Novartis exercised its call option to acquire Nestle's remaining 52% stake for $180 in cash consideration. Simultaneously, Novartis made an offer to minority shareholders for $153 in the form of an all-share offer of 2.8 Novartis shares. The first issue was that the offer was lower in monetary terms. The second issue was that it was in shares, which although technically fungible with cash, are worth less than an all-cash offer because they created uncertainty of what a minority shareholder would receive in the end. Moreover, the deal was further complicated because Novartis shares are priced in Swiss Francs, which introduced exchange rate risk for a minority shareholder. In short, the offer was inadequate any way you looked at it. Luckily, the three independent directors of Alcon formed a committee to review the transaction.

• January 20th, 2010 - Alcon's independent committee determined that the deal was "grossly" inadequate.

• February 17th, 2010 - RiskMetrics publicly stated that the Novartis deal was prejudicial to Alcon minority shareholders.

• July 8th, 2010 - Alcon's independent committee created a $50mm "litigation trust" that allowed them to continue to legally protect minority shareholder rights upon the acquisition of Nestle's 52% stake by Novartis.

• December 15th, 2010 - After a little over 11 months, Novartis folded their hand and agreed to acquire the remaining 23% in Alcon for a price of $168 per share. This is payable with 2.8 Novartis shares, and if the value of the share consideration falls short at closing, then it will be topped up to $168 with cash. The $168 consideration is basically the blended price that Nestle received for its two blocks of shares.

As always, there is some commentary that I would like to make. First and foremost, I find this deal to be bittersweet for minority shareholders. It is a positive outcome to this deal in the sense that the deal is finally getting done. It is negative in the sense that it has been a long time between the initial offer in January and the closing of the deal will be over a year, and closer to a year and a half once the legalities are wrapped up. Alcon shareholders have been in limbo, and will continue to be this way for the next few months.

Secondly, the bump in consideration from $153 to $168 is also positive. However, the consideration is in shares, which any appraiser can tell you are less valuable than cash. It is true that it will be a "tax free" rollover for shareholders, so they have the option of holding onto their stake without tax consequences. However, cash is a certainty and should always be valued higher than shares. Share values are transient. They are typically supported by fundamentals in the long-term, but can deviate significantly in the short-term. The other aspect of this transaction is that if the value of the offer comes in at more than $168 at closing, the share ratio will be reduced to ensure consideration remains at $168. Although I am skeptical of Novartis' share price rallying much higher prior to deal closing (due to hedging), the attractiveness of the consideration received will only be certain on the closing date. At current prices, Novartis is trading at 14x earnings, which is at the higher range of comparables, although not outrageous on an absolute basis. What I would be worried about as a potential Novartis shareholder is multiple compression, and more importantly, fund managers selling their newly acquired Novartis shares on the open market after the closing date, thereby depressing the price. In short, the consideration received is uncertain, and there is some probability of it being less than $168.

Third, the $168 is a blended price that Nestle received in total. It is a combination of an initial $143.18 on the 25% stake sold in 2008 and $180 on the 52% stake sold in 2010. I maintain that the $143.18 price was a trade done in the context of a different market and at a different time. As such, it is irrelevant to the pricing of any stake being sold in 2010. Moreover, the value of the Alcon business was different in 2008 than in 2010. I believe that the minority shareholders should have argued for $180, as they should receive the same consideration that Nestle received in 2010. At the very least they should have argued for an interest adjustment on the $143.18 portion, as Nestle effectively had access to that cash two years prior. My solution would have been to apply some sort of risk-free interest rate (t-bill or short-dated treasuries) to the $143.18 portion of the consideration calculation to bring the value of the cash to present value. Using one month US t-bills as the proxy, the additional consideration would amount to about $0.31 or 20 basis points more than what Novartis offered, primarily because rates cratered over the 2 year time frame. Although the methodology is more fair and correct (in my view), this option was probably not considered due to the minor amounts involved and the relative negotiating positions of Novartis and Alcon. On the flip side, I do understand that there is a control premium ascribed to Nestle's 52% block of shares, which minority shareholders cannot take part in. This is the main "bitter" aspect of the deal. The shares are probably worth $180, but minority shareholders have no legal way to force a bump. Nor can they argue that they deserve the price ascribed to a control block. Given that the independent committee has recommended that shareholders approve the deal, I believe it will go through as planned.

Fourth, I must applaud the independent board of directors for taking the steps necessary to fight for minority shareholder rights. The $15 increase in consideration for the 69mm shares held by minority shareholders translates into a little over $1bn in additional value that is rightfully theirs. That is the product of three individuals fighting for minority shareholders, but a slew of other parties as well. Both proxy advisory firms, Glass Lewis and RiskMetrics were instrumental in guiding the market to refuse Novartis' "grossly inadequate" initial offer.

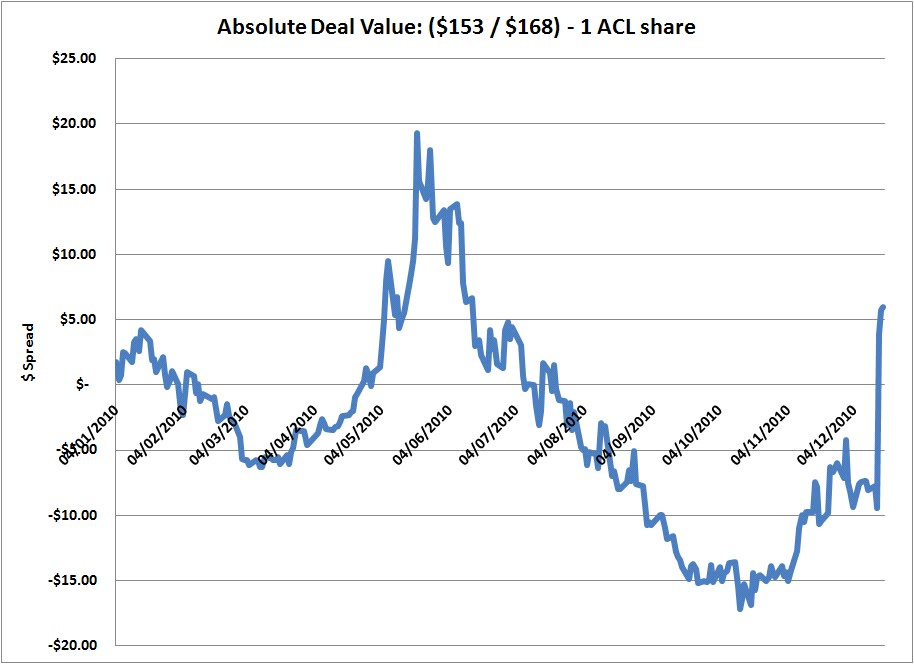

Fifth, as indicated by market folly's recent post, this deal will get done because of the fact that the arbs are now deep into this trade and will vote in favour. I wanted to point out visually how the market responded to this deal throughout time.

The graph shown above displays the spread value on a relative basis. What I mean by this is the spread value of the deal originally announced (the value of 2.8 NVS shares minus the value of 1 ACL share). As you can see, the market immediately priced a negative spread on the deal, as it believed that minority shareholders should get closer to $180 for their shares. Three things are playing out here. First, the ACL shares are initially being hedged with NVS shares as arbs have to short 2.8 NVS for each 1 ACL they own. That put tremendous pressure on the price of NVS in the market, thus lowering the value of the share consideration immediately. This is in addition to the share dilution concern by NVS shareholders who would have sold NVS for that reason alone. Second, as markets began to tumble in the summer, NVS shares had more pressure on them which pushed the value of the share consideration down even further and the expectation of a bump in the share exchange ratio up. Hedgies would look at the value of the share consideration at $135 and say that it is too low relative to the already low absolute valuation of $153 that was set by NVS only 6 months prior (keeping in mind there is relatively little change in the fundamental value of the business). They would also assume that they are getting a free option on a bump in the share exchange ratio, and would thus put on the spread at +$5 all the way up to $20. Third, as market participants talk and determine what the real value of the minority stake is and the likelihood of a bump, their expectations for a bump increase simultaneously (along with the risk trade being put back on in August) and they begin to push the value of ACL shares from the $150's into the $160's. The interesting aspect of this is two-fold. First, given what market folly indicated in his post, the hedgies could have been colluding to go long at the same time and thus affect the status of the deal (a form of quasi-activism). The second interesting aspect is that as soon as the stock continues to hang at the $160 level for an extended amount of time, it is clear to any market participant that NVS will be forced to offer more consideration if it wants to close the deal - in essence, the bump is a self-fulfilling prophecy. You can see this in the chart below. From August onwards, the deal traded at a negative spread (assuming a $153 payout), with ACL rallying all the way to $170, presumably under the assumption by some poor-sap that a deal would get done at $180. It promptly sold off to a more reasonable level in the low 160's when NVS decided to bump to $168 to get the deal done.

Sixth, strategic deals like this always get done in the end. Novartis is primarily concerned with acquiring and running the business for fundamental / strategic reasons. They could not continue to fight to oppress minority shareholders because they have the business to run as control investors. I understand that they tried to take advantage of minority shareholders, however, I am just baffled at how long it took for them to work out the deal. You can clearly see them integrating the business as time goes on (appointment of Novartis CFO to oversee Alcon, appointment of Novartis CEO to chair Alcon, etc), so you can see their thought process playing out in the press releases, and it was apparent to me that they were going to do the deal at some point in time. Why did it take eleven months? I guess we'll never know.

Seven, it took NVS approximately 8 months to acquire Nestle's 52% stake, and my assumption is that it will take a shorter time frame to acquire the minority stake held by the public. The company has guided to "the first half of 2011" in terms of closing, which makes it a 6 month long wait until consideration is paid out, assuming a worst case scenario. I think there is a chance it could get done sooner. From a risk-arb perspective, that is a long time to have your capital at risk, which will not be attractive to all arbs. The share price of ACL should stay within hailing distance of $168. At the current price of $161.70, the annualized return is roughly 8%, which is about right for this type of trade. I think ACL has to trade down to $157 or $158 to make it attractive currently. With that said, I think there will be an opportunity at some point in time to go long ACL at an attractive annualized return (+15%). Given the volatility in the markets and the skittishness of arbs, there is a good chance of ACL being sold off in the coming months due to the risk trade being taken off by funds. As it stands right now, I'm a buyer at $158.

Just a few points to add, since the deal will only require SEC and shareholder vote the timing is probably more like early April. The holidays may delay the filing process. One of the factors that drove acl down the day after the deal was announced was the treatment of the cash component in the event that NVS averages below 60 during the pricing period (the cash top up) which is supposed to bring the value up to 168. In reality the floor price will be adjusted lower in the event the average is below 60 to account for the regular cash dividend NVS will be paying. The adjustment will be paid in shares equal to the difference between the average price of nvs and 60 to a maximum of the dividend divided by the ave price. That aside, anything below this will be paid in cash that will be treated as a dividend according to the Swiss tax treaty with the US and subject to up to 35% witholding. Holders domiciled in countries without a tax treaty (offshore funds) could be subject to the full 35% witholding. This doesn't affect pensions which can apply to get the 35% back, and investors from countries with a tax treaty who can apply to reclaim 20% of the witholding and then most likely deduct the remaining 15% against foreign gains. In theory the implied short put in NVS due to the tax drag can be bought back ( the estimated March div is about 2.50 and there's an Ap 57.5 put trading). Bought on ratio depending on your estimate of the tax drag you should be able to offset the tax hit but you have to add the cost to your trade. Of course if NVS is above 60, it could all be for nothing.

ReplyDeleteAs for hedging in NVS you probably don't want to worry about that until the pricing period.